Financial year end is fast approaching

and many end users of Derivatives still grappling with issues of component of

Fair Value for a Derivative on their Balance sheet. Many of you are Corporate Treasurers,

Auditors or valuation personnel at financial institutions who are asking

questions like why OIS discounting, CSA discounting, should I need to apply CVA

and DVA, am I being charged for FVA etc. Debate around some of these like what

discounting approach, (OIS vs Libor) has been settled in terms of calculating

the discount curves and methodologies. Items like FVA have been the hot topic

for last few months. In this article, we show general characteristics and

context around these issues.

An evolving environment

The global financial crisis ushered in

a new era of increased regulatory scrutiny. In this new environment, regulators

have, and continue to implement a host of new laws and rules to prevent a

repeat of the crisis. Implementation of regulations namely, the Dodd-Frank Act,

Basel III framework constraining financial institutions in their strategic

choices by increasing capital and liquidity requirements and will face higher

costs in providing financial products to their consumers. During the period of credit expansion that

preceded the financial crisis corporate consumers were able to expand

activities on the wave of cheaper credit extended by banks due to under pricing

of liquidity and funding costs. Banks were universally pricing financial instruments

like derivatives by discounting future cash flows at LIBOR. If these cash flows

are not risk free then they will be adjusted by CVA. Financial crisis has

illustrated that OIS rate (which

is weighted average of overnight unsecured lending rates in US interbank

market) not LIBOR is risk free rate due to

embedded credit risk. Also, banks cannot possibly borrow and lend at LIBOR due

to funding risk. Now derivative pricing is undergoing revolutionary changes.

Credit and liquidity risks those were negligible in pre-crisis period were

addressed by including, credit risk, collateral and funding to measure fair

value of an instrument. Having set this context, as a user of financial

instrument you need to understand how valuation has changed from the world of

simple LIBOR discounting to a new world of OIS discounting with various

valuation adjustments. This understanding is imperative to know cost drivers of

the value of a derivative product and helps you to make an informative decision

in transacting them.

Changing the way you do

business

Derivative

valuation primarily comprises of forecasting cash flows and then discounting

these cash flows to current day and applying various valuation adjustments.

Anatomy of Fair Market Value

Risk Free Value: Fair market Value of a derivative

using risk free rate

CVA:

Credit Valuation adjustment is adjusting the fair value due to loss arising

from the default risk of the counterparty

DVA: Debit Valuation adjustment is adjusting the

fair value due to loss arising from the own default risk of the entity

FVA: Funding Valuation adjustment to fair value

to account for funding costs

Coll Va:

Adjustment to fair value to account for difference in the value of derivative

in risk free rate discounting vs actual CSA discounting

Risk Free Value:

Before the 2007 dealers, as well as

their regulators and auditors viewed fixed rates on LIBOR swaps to be a

reasonable and workable proxy for the risk free yield curve and this task was

quite simple. For a LIBOR based interest rate swap cash flows are projected and

discounted using a LIBOR curve. 2008 financial crisis has illustrated the

credit risk in LIBOR curve clearly and replaced it with OIS rate. OIS rate is

Fed funds rate which is weighted average of overnight unsecured lending rates

in US interbank market. This rate due to overnight tenor carries least amount

of credit risk. At the peak of crisis OIS-Libor swap spreads widened from 5-7

bps in pre-crisis period to 350bps. Typically, for a collateralized derivative

with daily margining OIS rate is specified in CSA (credit support Annexe).

Hence OIS rate with its least embedded credit risk and underlying funding rate

for collateralized derivatives is suitable rate for risk free valuation.

Within OIS discounting valuation framework, cash flows are projected using

Libor curve and discounted using OIS curve to calculate risk free value. Once

risk free value is determined, banks add the cost of counterparty credit risk

to adjust the value of the trade if cash flows are not risk free by adding credit

valuation adjustment (CVA). Hence a high risk corporate will have to pay higher

cost for entering into trade with an institution compared to low risk

counterparty. In a world where all

counterparties use CVA will never agree on one price for a trade. Debit

valuation adjustment (DVA) took it genesis from considering bilateral CVA

(BCVA). Therefore Risk free value is adjusted for default risk arising from the

institution (DVA) and their counterparty (CVA) and accounting for credit risks

in the valuations that were not considered in pre-crisis period.

Funding Valuation

Adjustment

Corporations and other non financial

entities use derivatives to manage their cash flow operations and they do not

post daily collateral and hence called Uncollateralized Derivatives. Banks aim

to run hedged books therefore hedge these uncollateralized derivatives with

collateralized trades face collateral and funding costs. Institutions

are accounting for collateral and funding costs via funding valuation

adjustments to the risk free value.

Bank

A simultaneously enters into an offsetting hedge swap with another Bank B. Bank

A has to post and receive collateral on this hedge swap whenever the hedge swap

has negative market value and positive market value respectively.

Negative Market Value:

When hedge swap has negative market value client swap will have positive market

value. Bank A has to post collateral. In this case bank borrows funds at banks

unsecured borrowing rate and posts collateral that is earning OIS rate.

Positive Market Value: When

hedge swap has positive market value client swap will have negative market

value. Bank A receives collateral that is earning OIS rate.

Bank

A is in a situation where it has to borrow funds at its funding rate to post

collateral. At the same time collateral earns OIS rate creating an asymmetric

situation. Due to this Bank A has to adjust the market value of the swap with

funding valuation adjustments (FVA). FVA

accomplishes the goal of adjusting the funding costs that are not accounted by

OIS valuation.

Conclusion: Derivative

products that are collateralized should be

1) Discounted by

appropriate collateral yield curve

2) Apply CVA and

DVA to measure and adjust its Value

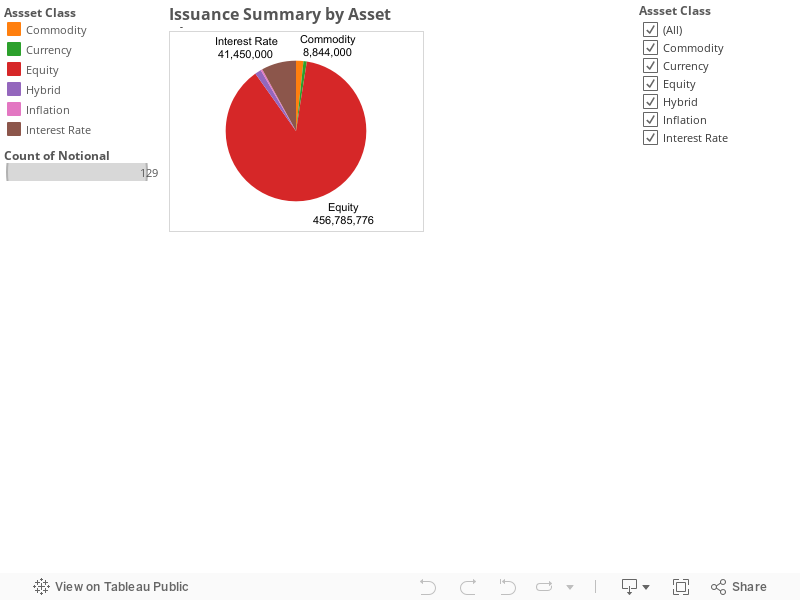

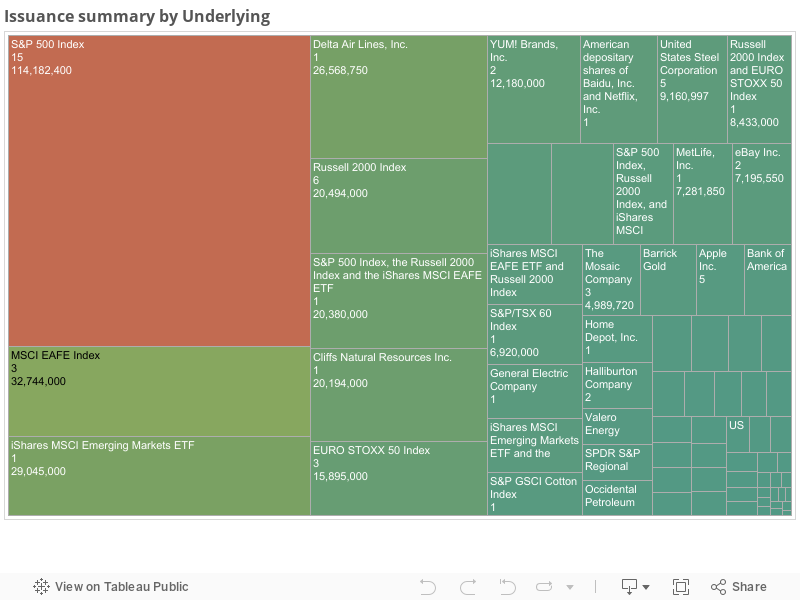

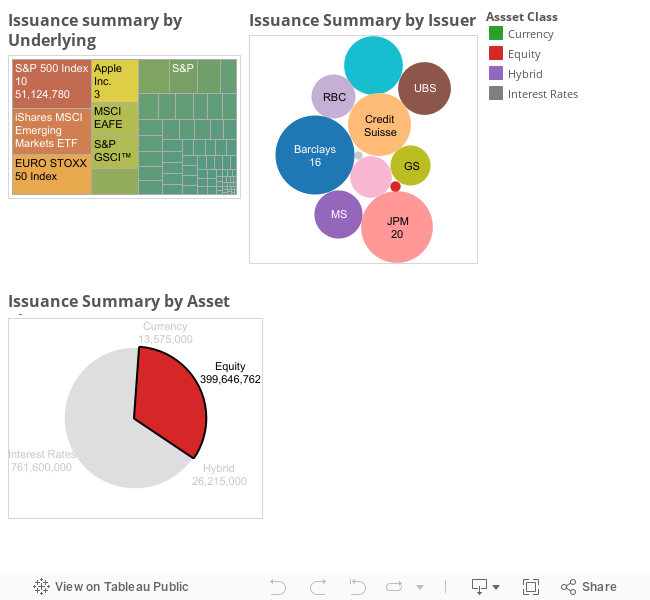

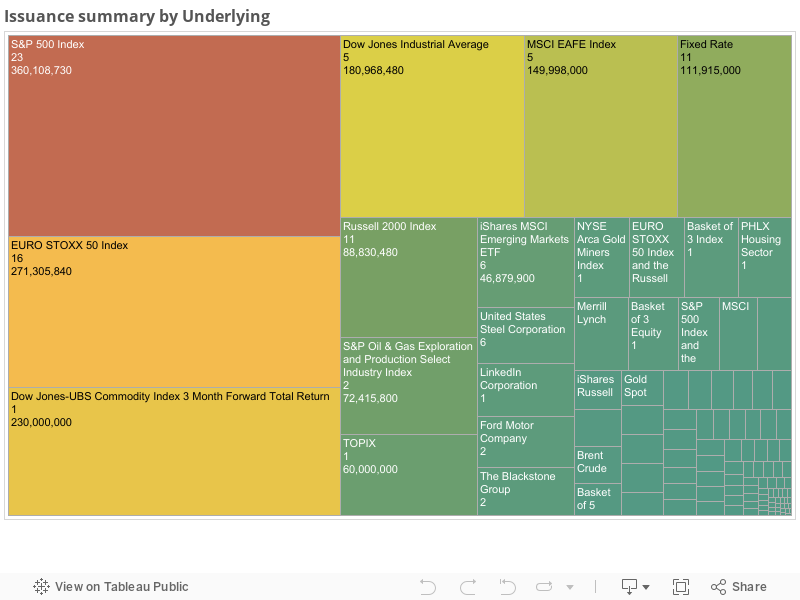

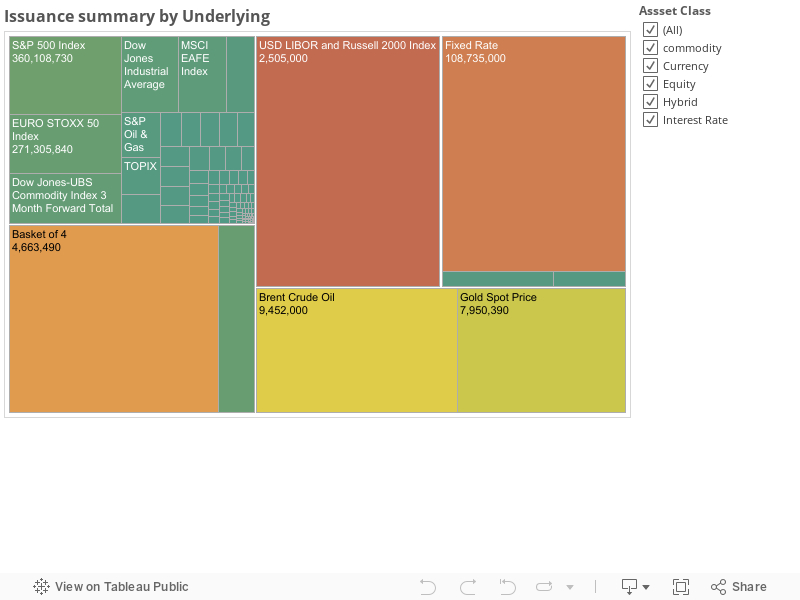

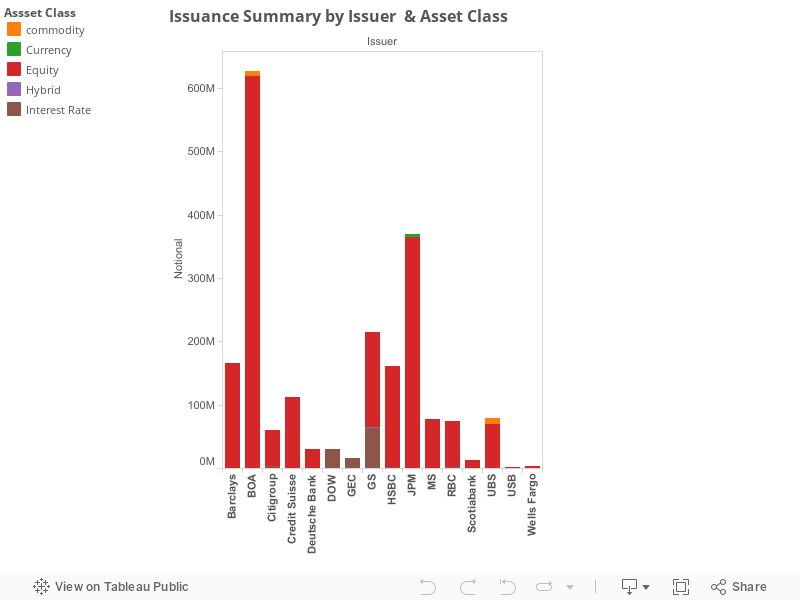

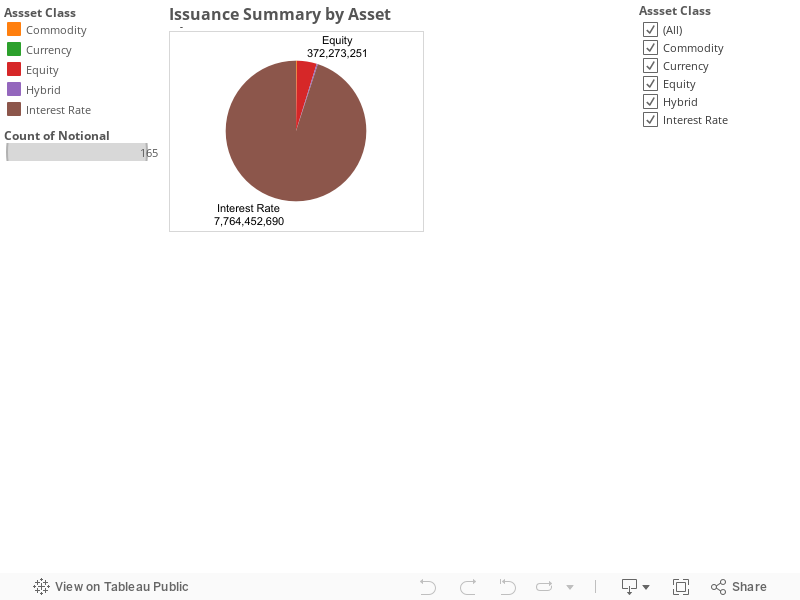

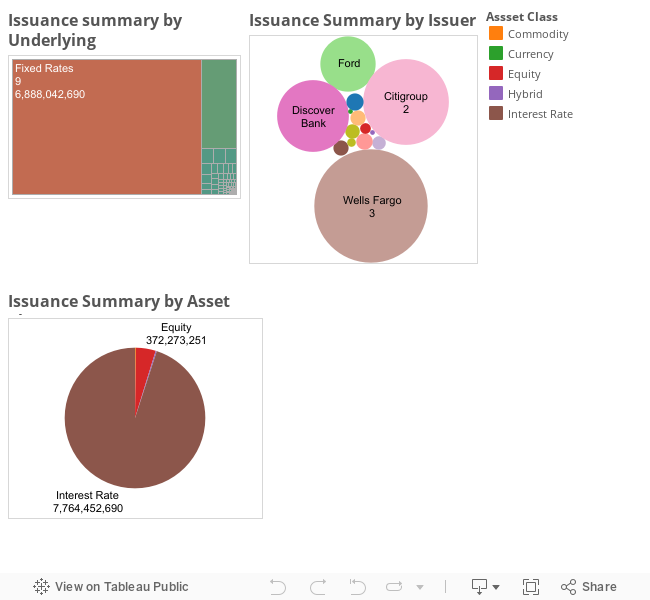

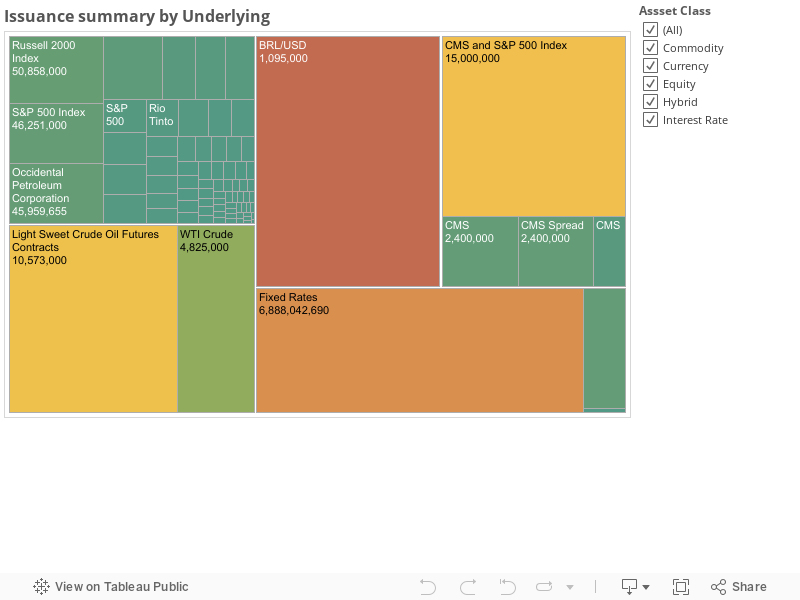

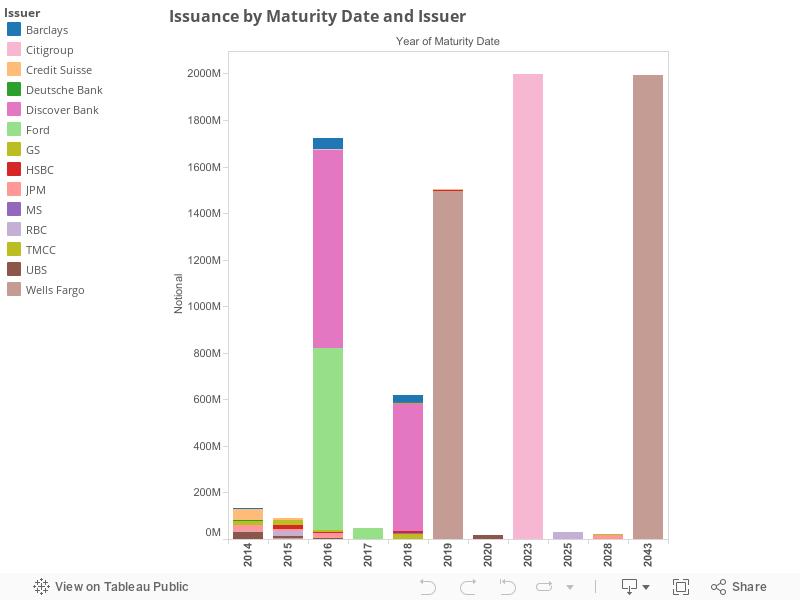

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

Underlying analysis

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

Underlying analysis

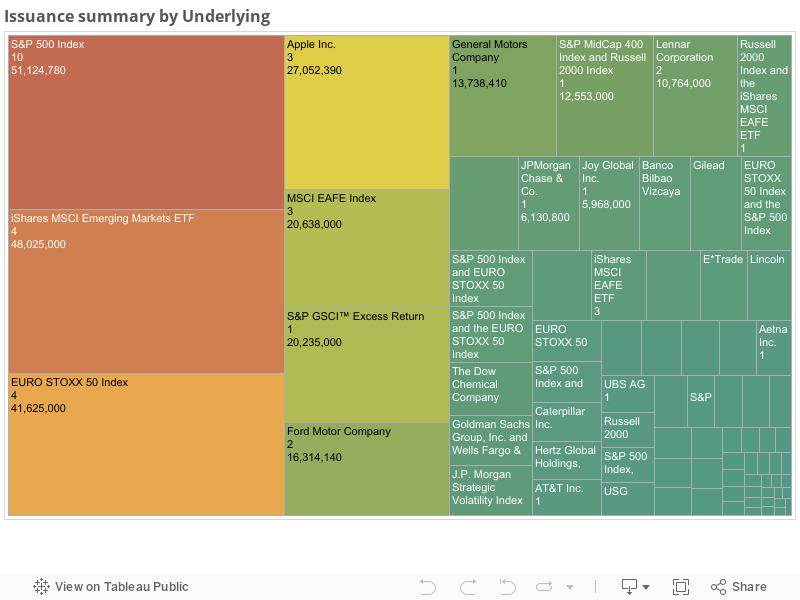

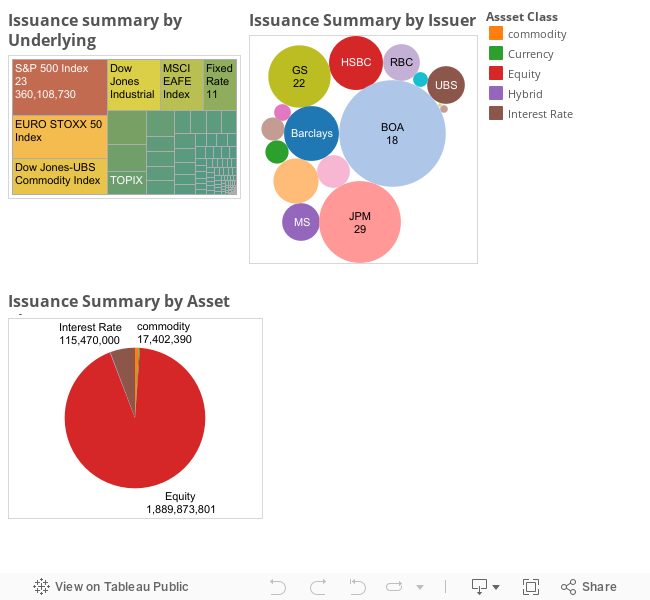

On the Equity linked notes front there has been strong activity. Notes have been created on variety of underlyings. Index related issuance has been significant. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Zillow, Hess Corporation, Occidental Petroleum Corporation, Baidu, Inc)

Notable notes this week were tied to Occidental Petroleum Corporation (46 MM) issued by Credit Suisse. This note belongs to the class of leveraged and Yield Enhancement type. Morgan Stanley created a note Cusip:22539T555with a size of 46 MM paying 8% coupon income.On the upside this note pays 65% appreciation in the underlying. On the downside this note is protected beyond 80% decline in the underlying.One reason to participate in this kind of note is you are getting 8% coupon return. Another deal created by JPM on Zillow company Cusip:48126NYN1 belongs to Reverse convertible type. This note provides 17.25% return with principal at risk.

On the Equity linked notes front there has been strong activity. Notes have been created on variety of underlyings. Index related issuance has been significant. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Zillow, Hess Corporation, Occidental Petroleum Corporation, Baidu, Inc)

Notable notes this week were tied to Occidental Petroleum Corporation (46 MM) issued by Credit Suisse. This note belongs to the class of leveraged and Yield Enhancement type. Morgan Stanley created a note Cusip:22539T555with a size of 46 MM paying 8% coupon income.On the upside this note pays 65% appreciation in the underlying. On the downside this note is protected beyond 80% decline in the underlying.One reason to participate in this kind of note is you are getting 8% coupon return. Another deal created by JPM on Zillow company Cusip:48126NYN1 belongs to Reverse convertible type. This note provides 17.25% return with principal at risk.

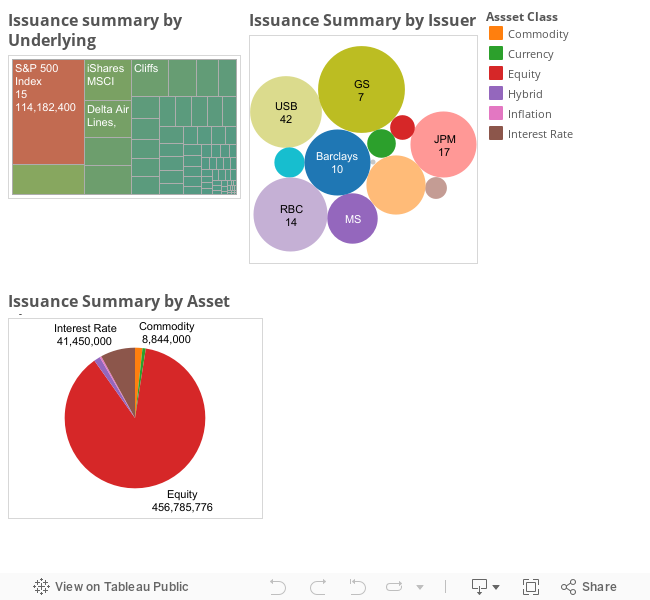

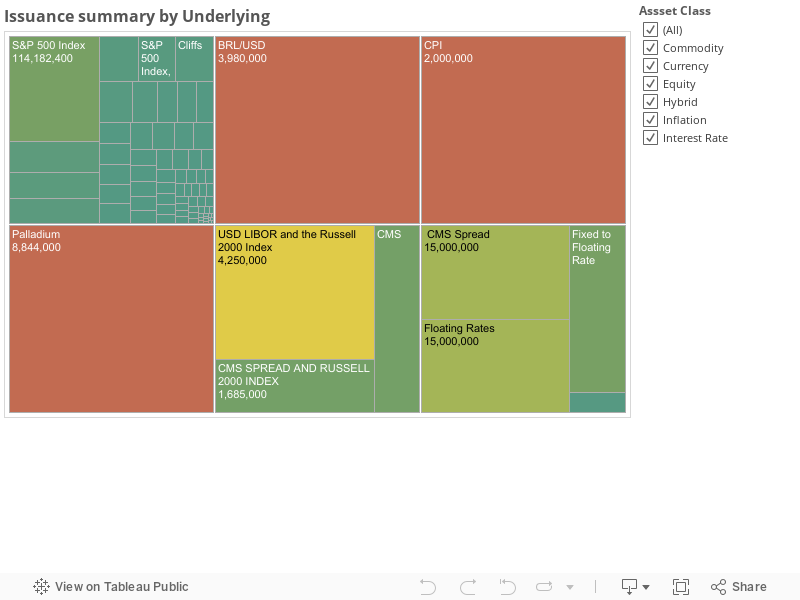

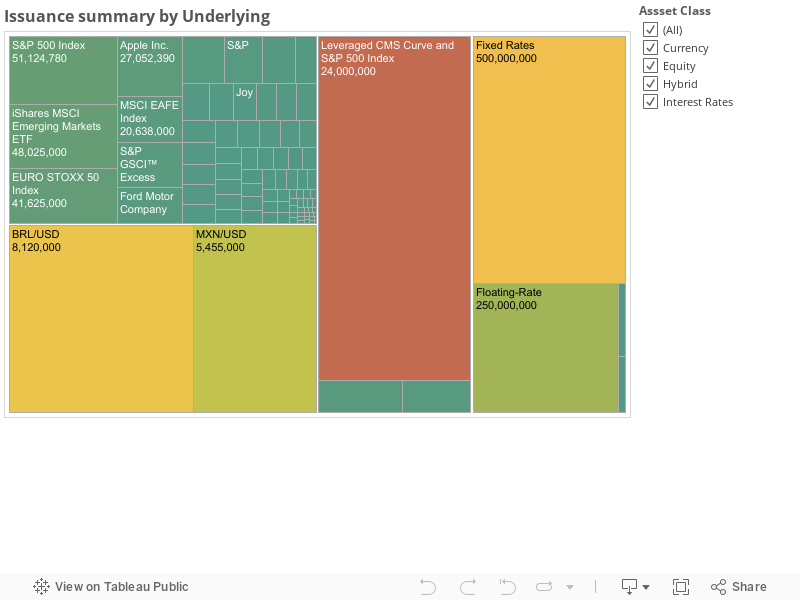

Interest rate linked issuance limited to standard, step up callable notes and Fixed rate notes. Activity has been subdued this week.Citigroup, Wells Fargo and Ford motor are major issuers of these products.

There has been some issuance activity in Currency segment of the markets. Goldman issued note linked to BRL with protection on losses up to 30% depreciation in the BRL exchange rate and potential to gain 30% if the currency appreciates above 3%.

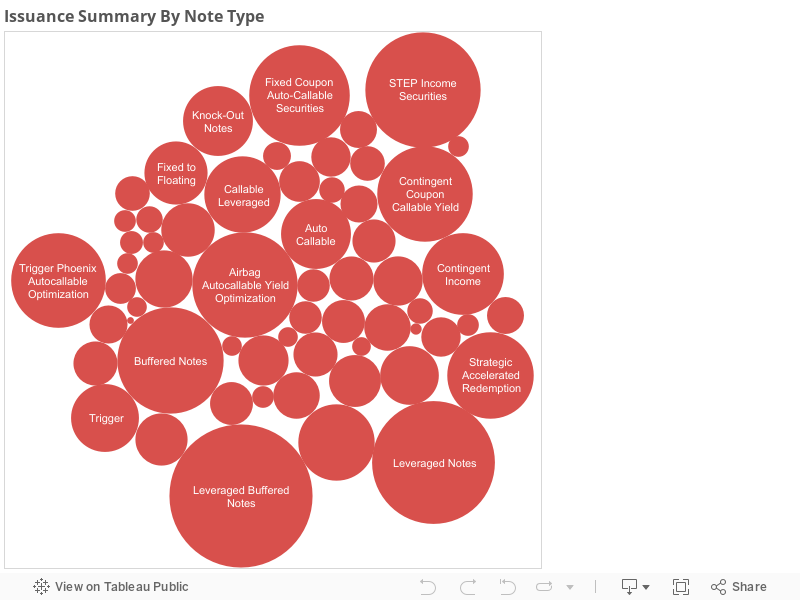

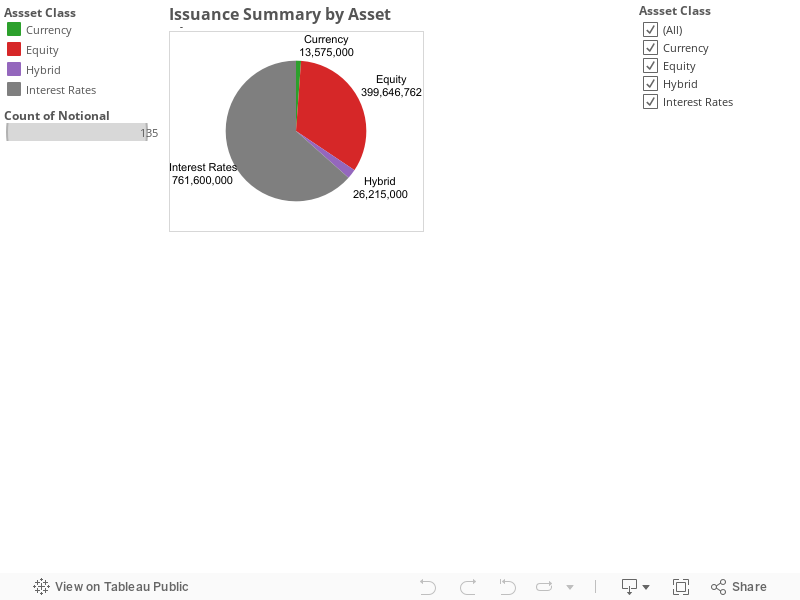

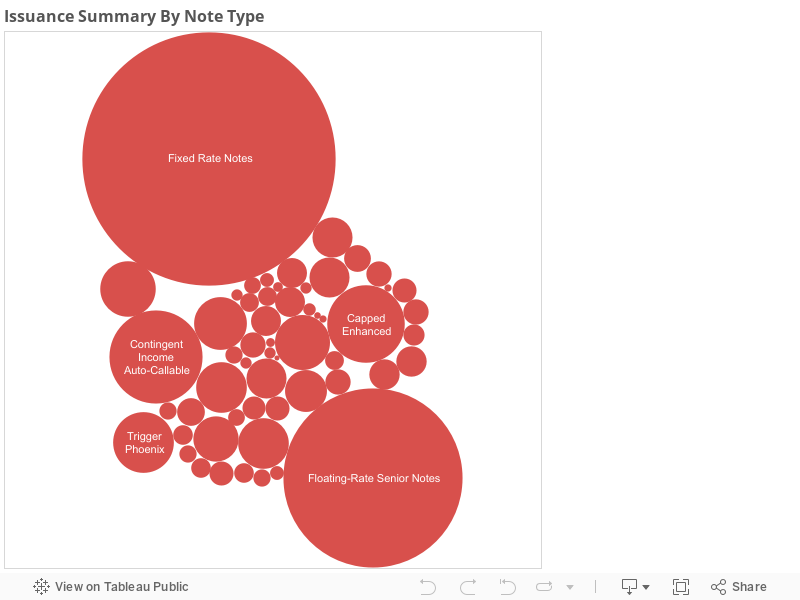

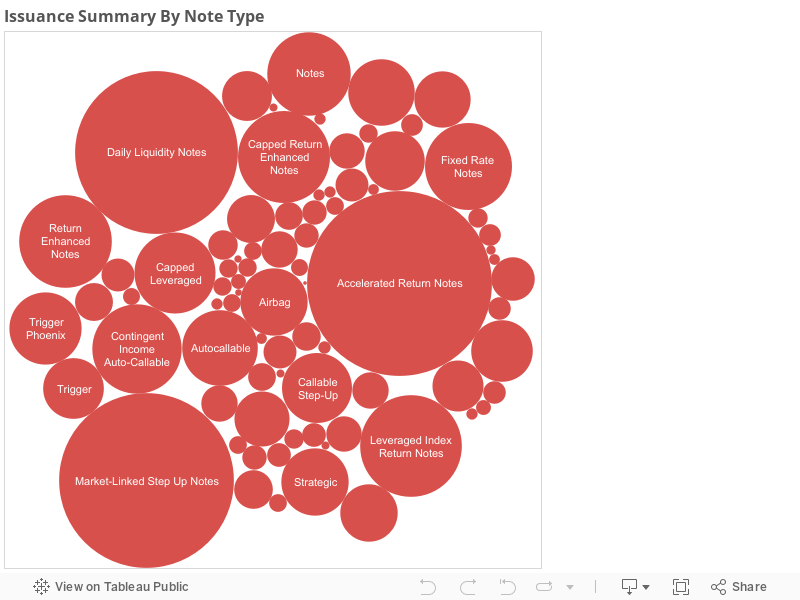

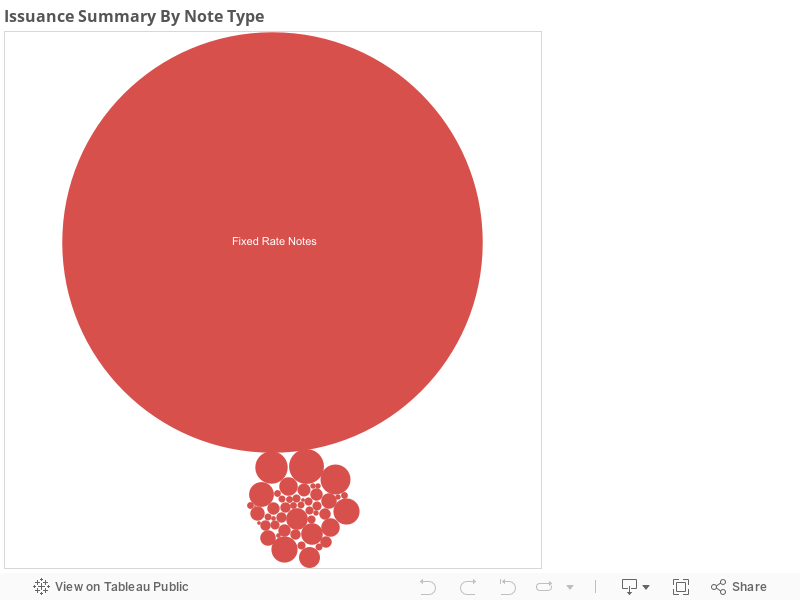

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Interest rate linked issuance limited to standard, step up callable notes and Fixed rate notes. Activity has been subdued this week.Citigroup, Wells Fargo and Ford motor are major issuers of these products.

There has been some issuance activity in Currency segment of the markets. Goldman issued note linked to BRL with protection on losses up to 30% depreciation in the BRL exchange rate and potential to gain 30% if the currency appreciates above 3%.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been interest rate linked notes.

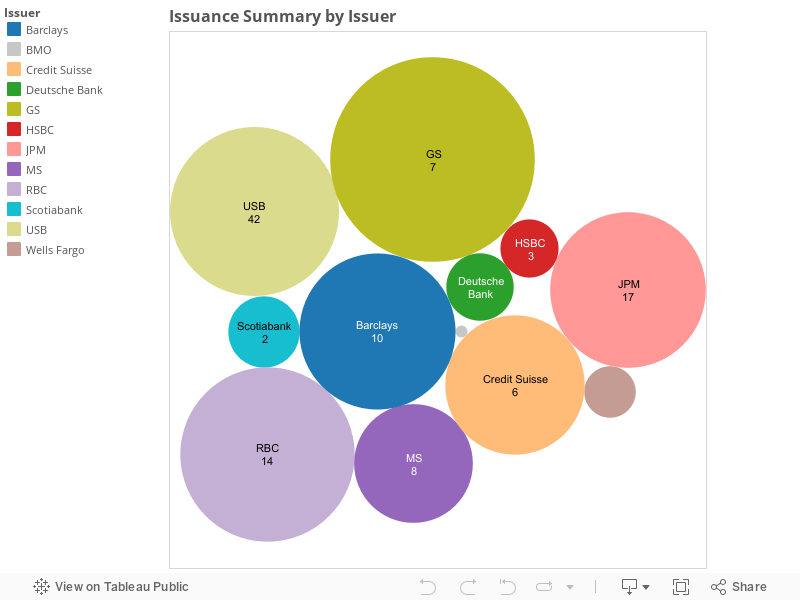

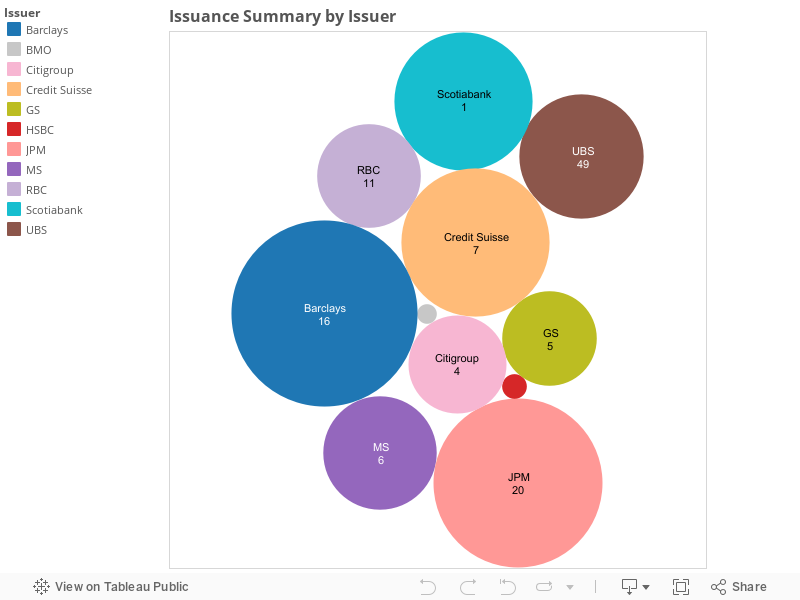

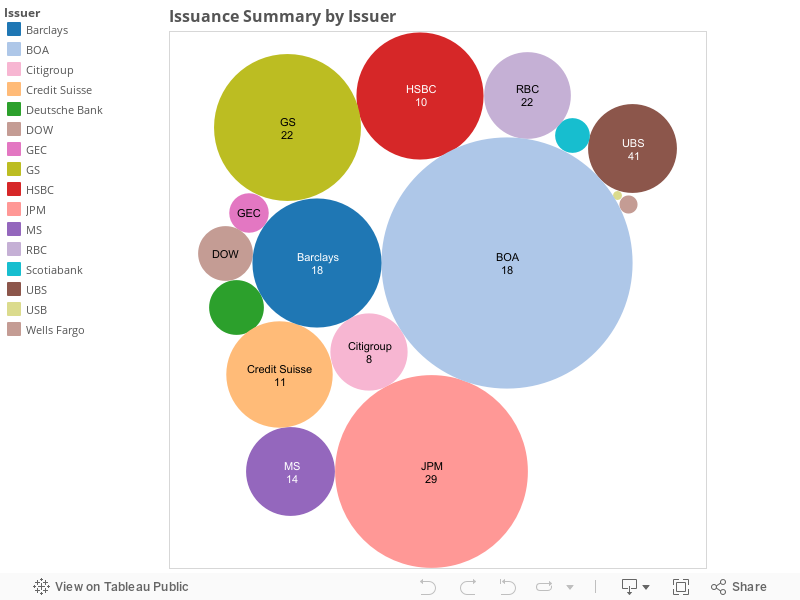

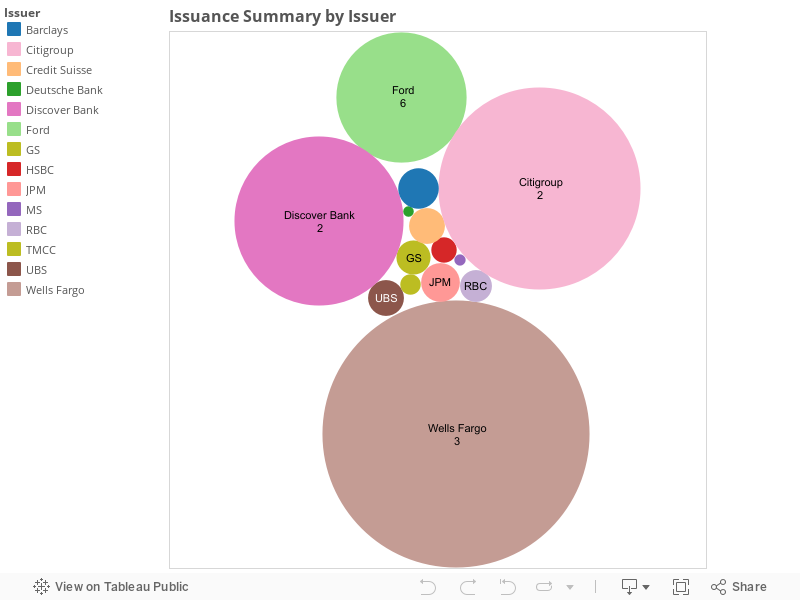

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week UBS, MS, GS and Barclays captured issuance market share.

Popular notes have been interest rate linked notes.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week UBS, MS, GS and Barclays captured issuance market share.

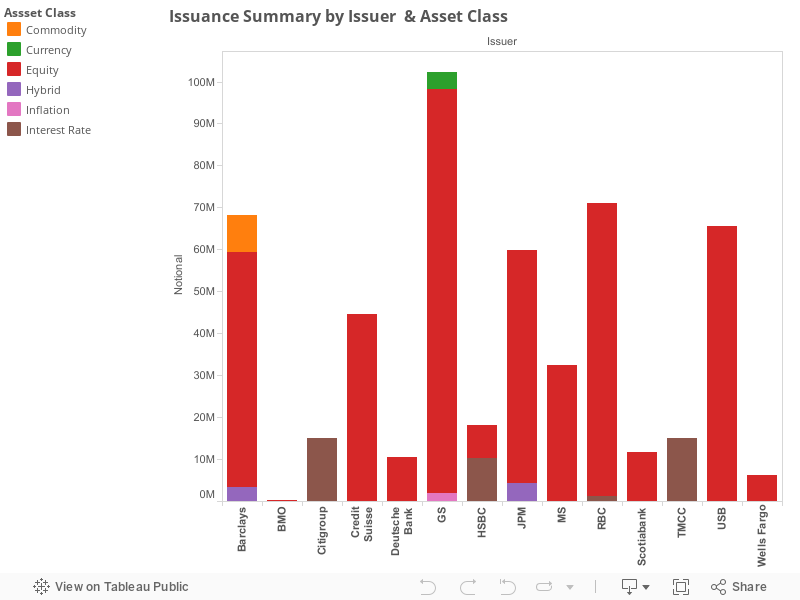

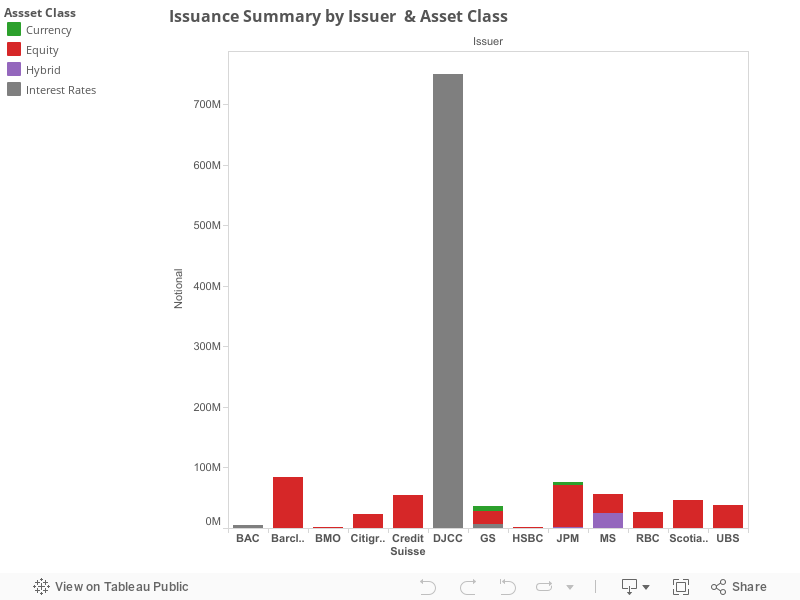

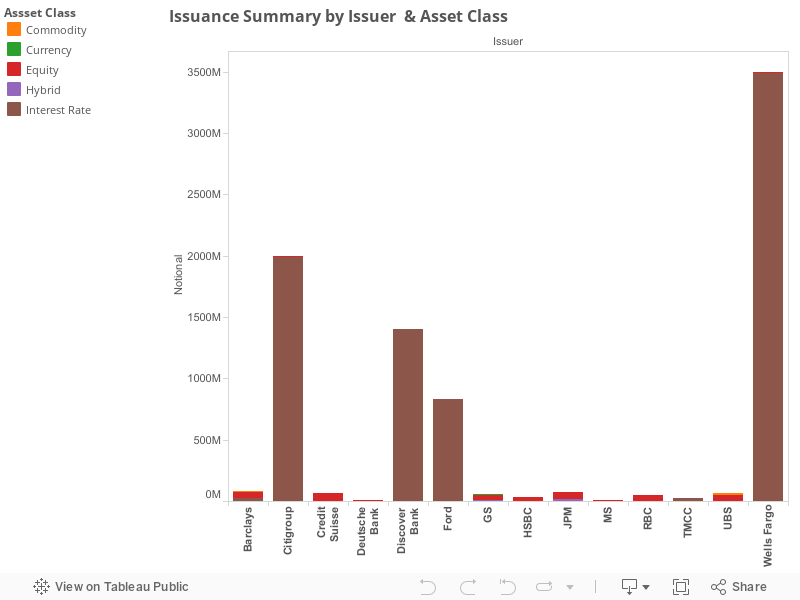

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

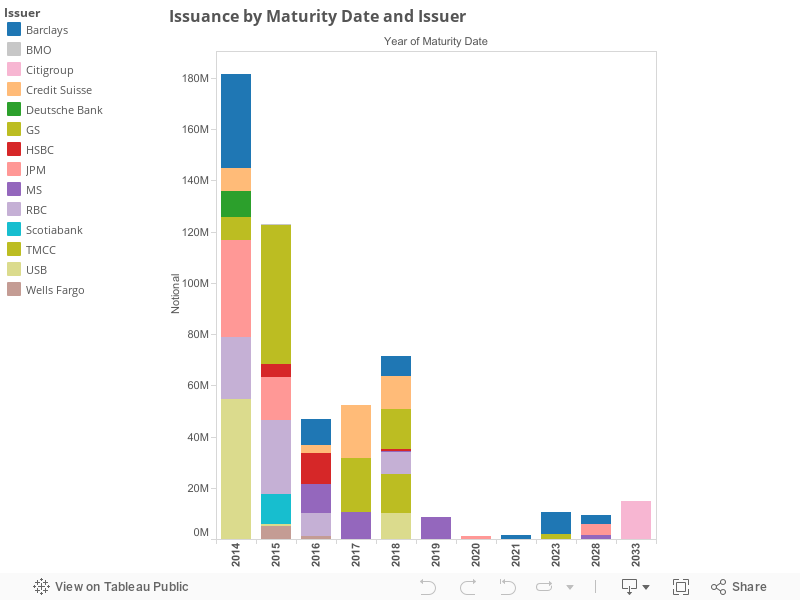

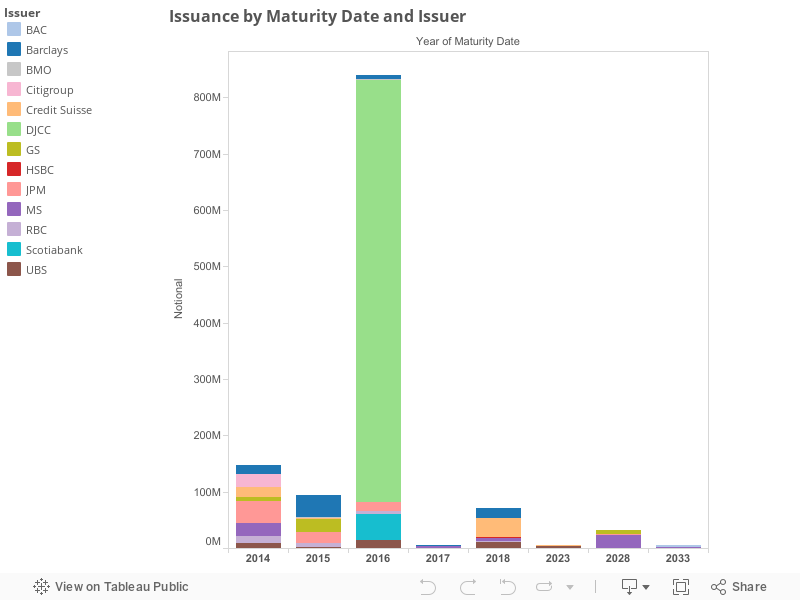

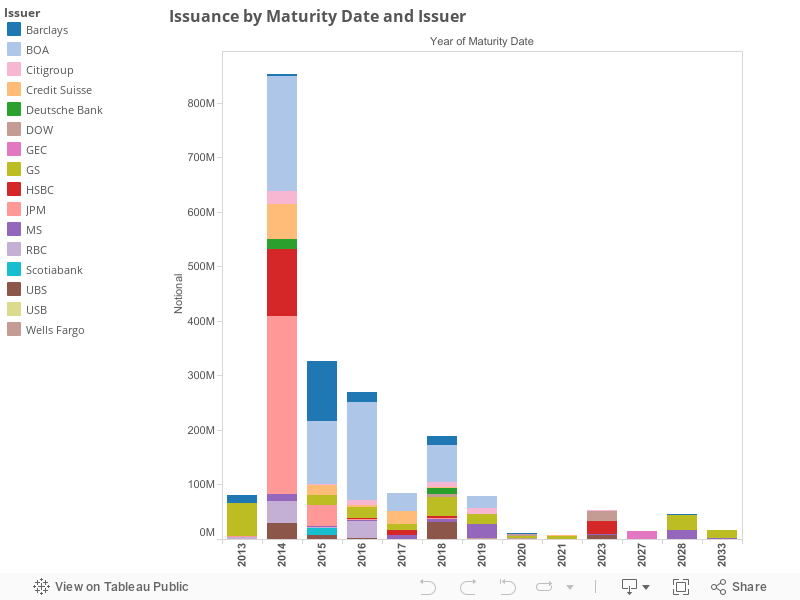

For additional details please refer to the Issuance summary table.

For additional details please refer to the Issuance summary table.