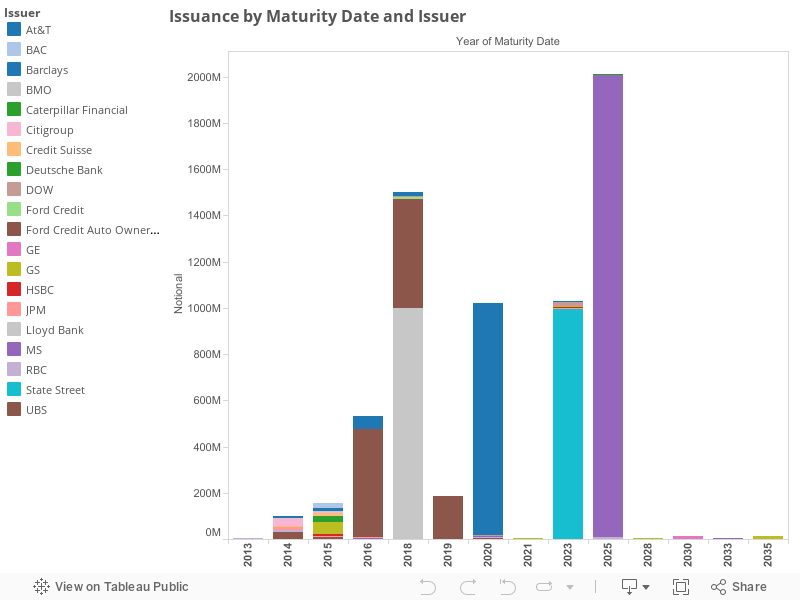

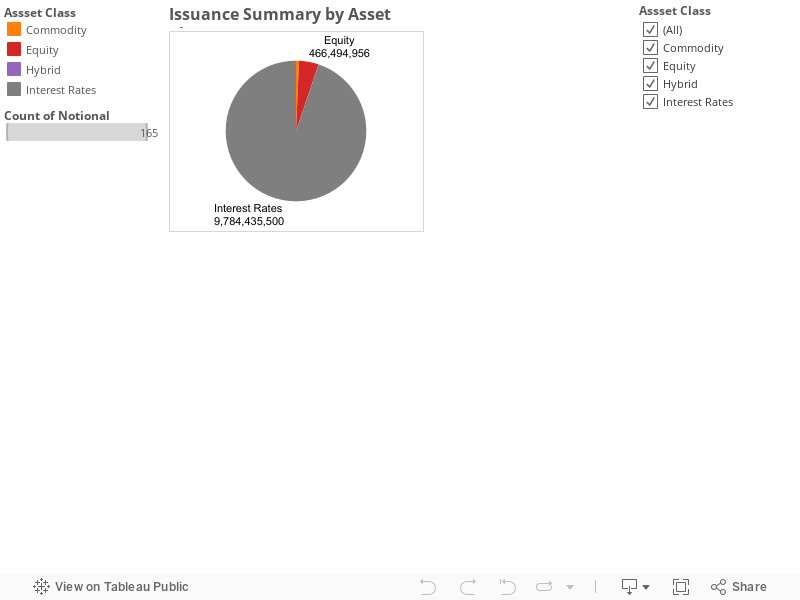

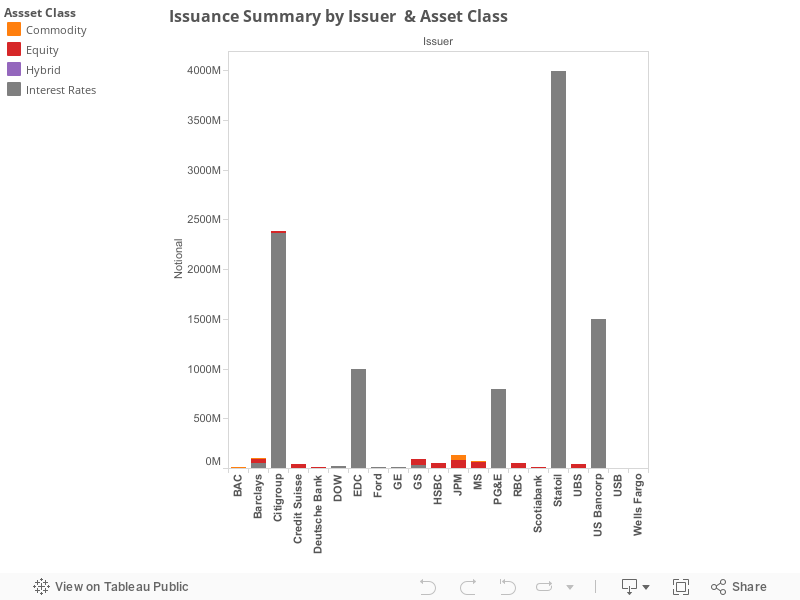

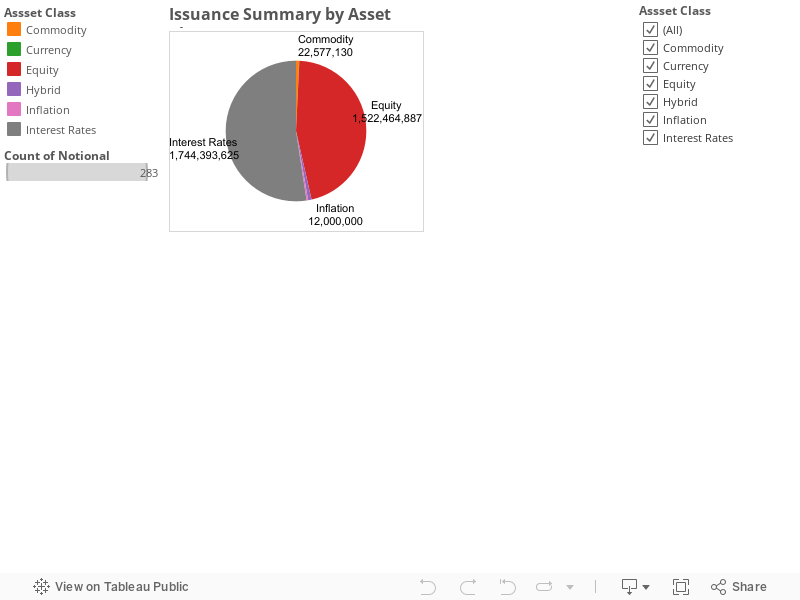

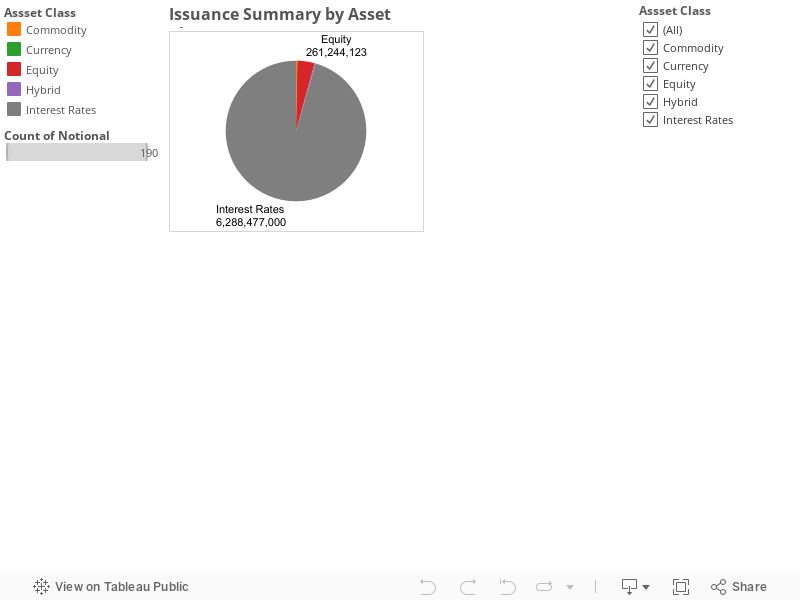

During the week of November 18-22, 2013 structured note issuance has been 6.8 Bn across various issuers and asset classes. Most of the issuance (260 MM) is driven by Equity Linked notes and 6.5 Bn of the issuance is driven by Interest linked products. There has been some activity in commodity linked issuance this week. For Details of the distribution refer to the chart below. Not surprisingly majority of the structured note issuance is linked to Interest rate linked by few issuers.

This week, structured notes were issued with variety of flavors and interesting themes. Majority of this issuance comprised of Interest Rate related notes Read on for more details.

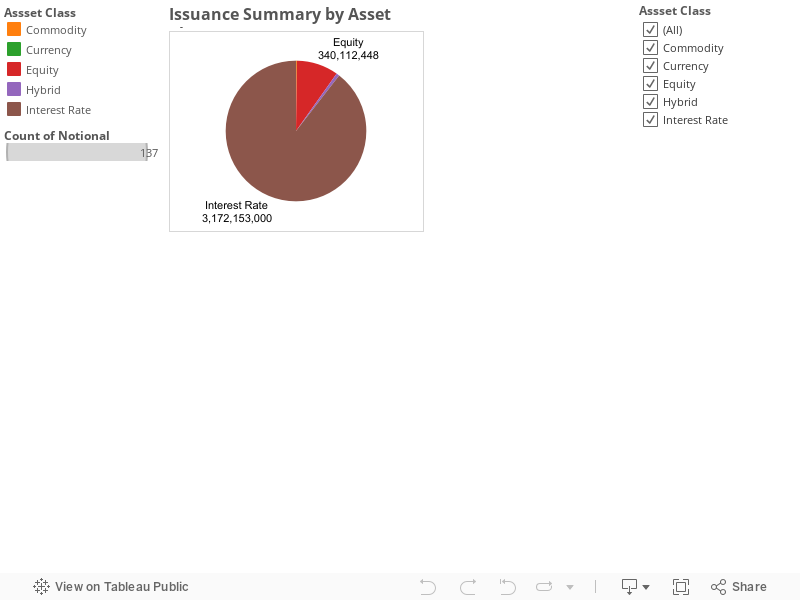

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

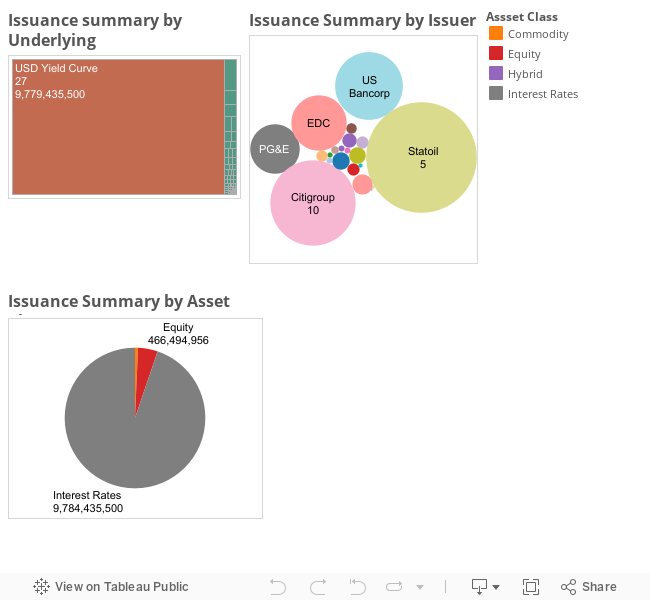

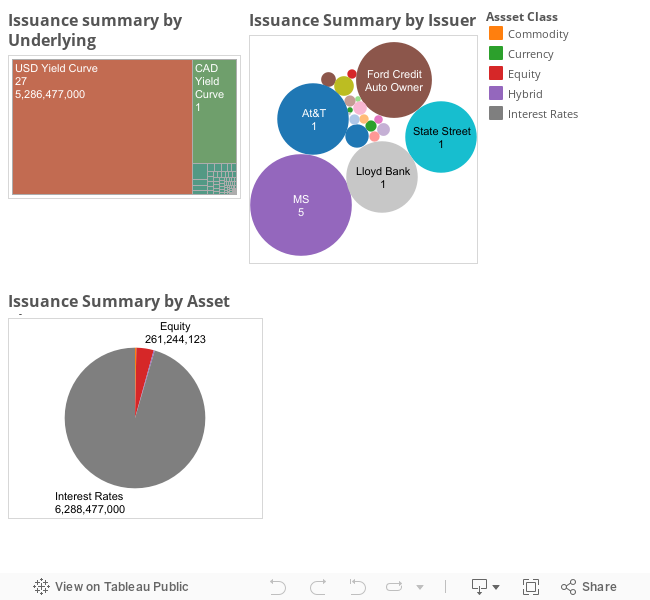

Underlying analysis

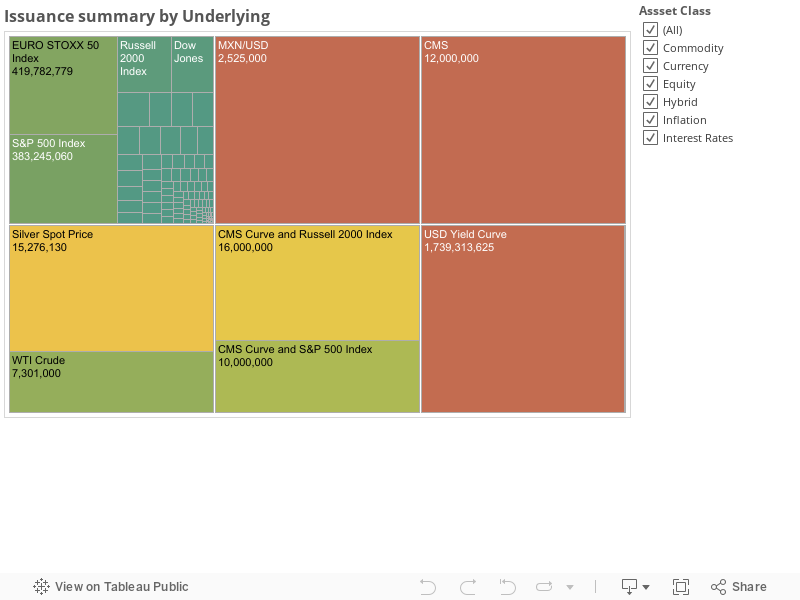

On the Equity linked notes front there has been strong activity. Notes have been created on variety of underlyings. Index related issuance has been significant. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Pulte group, Apollo Management, Face Book, Rackspace Hosting, Best Buy and so on). There has been significant activity around Apollo capital management. Looks there is high appetite from institutional investors to conduct their portfolio balancing process.

Notable notes this week were tied to Apollo Capital management Stock (6.5 MM) issued by UBS. This note belongs to the class of Yield Enhancement type. UBS created a note 90271R400with a size of 6.5 MM paying Market performance at maturity date (11/24/14). On the downside this note is exposed to one to one downside underlying performance beyond the Trigger level. One reason to participate in this kind of note is you will get a positive returns as long as the underlying is above the trigger level on the downside also. This is a good deal for risk averse investor.

Underlying analysis

On the Equity linked notes front there has been strong activity. Notes have been created on variety of underlyings. Index related issuance has been significant. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Pulte group, Apollo Management, Face Book, Rackspace Hosting, Best Buy and so on). There has been significant activity around Apollo capital management. Looks there is high appetite from institutional investors to conduct their portfolio balancing process.

Notable notes this week were tied to Apollo Capital management Stock (6.5 MM) issued by UBS. This note belongs to the class of Yield Enhancement type. UBS created a note 90271R400with a size of 6.5 MM paying Market performance at maturity date (11/24/14). On the downside this note is exposed to one to one downside underlying performance beyond the Trigger level. One reason to participate in this kind of note is you will get a positive returns as long as the underlying is above the trigger level on the downside also. This is a good deal for risk averse investor.

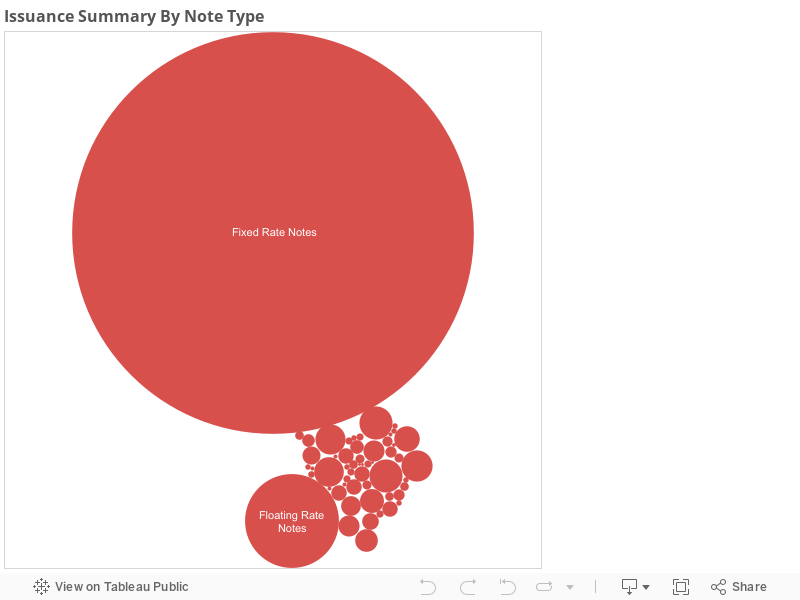

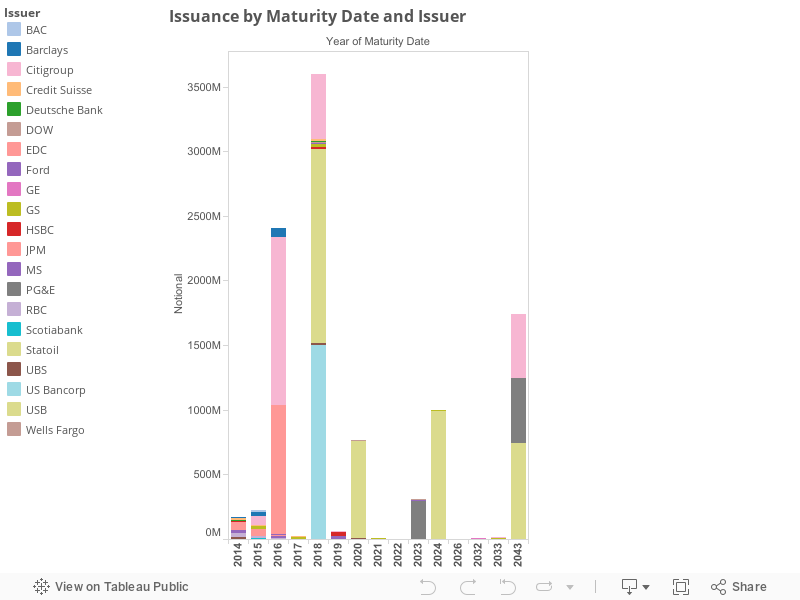

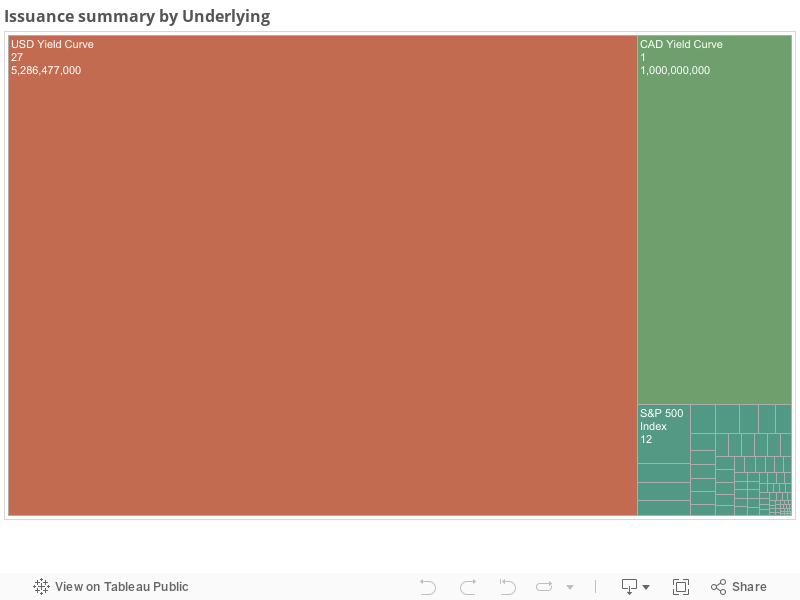

Interest rate linked issuance limited to standard, step up callable notes and Fixed rate notes. Activity has been subdued this week.Citigroup, Wells Fargo are major issuers of these products. AT&T has issued CAD 1 Bn Fixed rate Note to the investors.Interestingly this note is one of the largest notes issued to the investors.

This week we have seen commodity note issuance tied to WTI crude oil. There has been a Currency linked note tied to USDMXN peso us issued by Goldman.

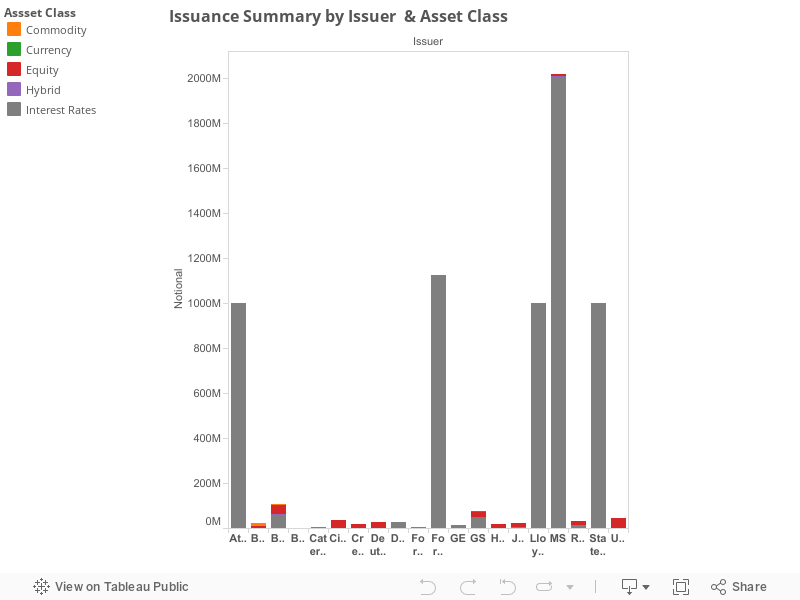

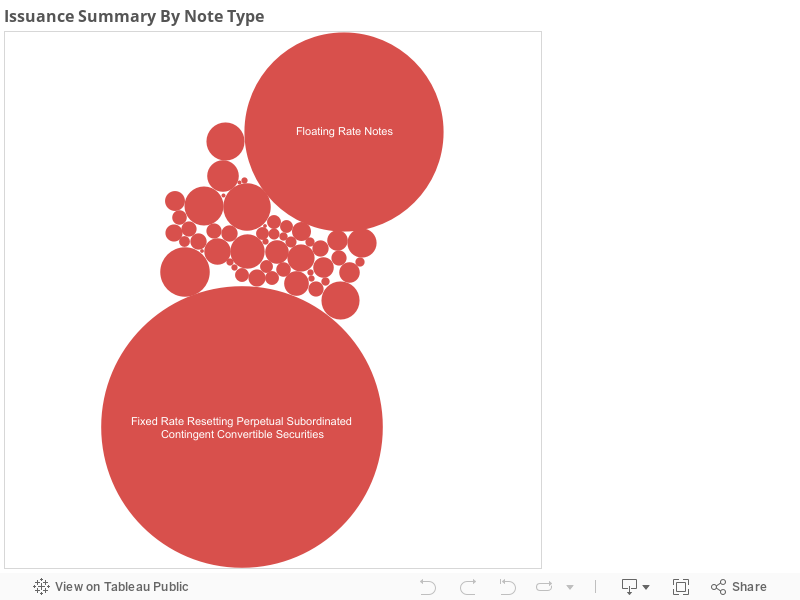

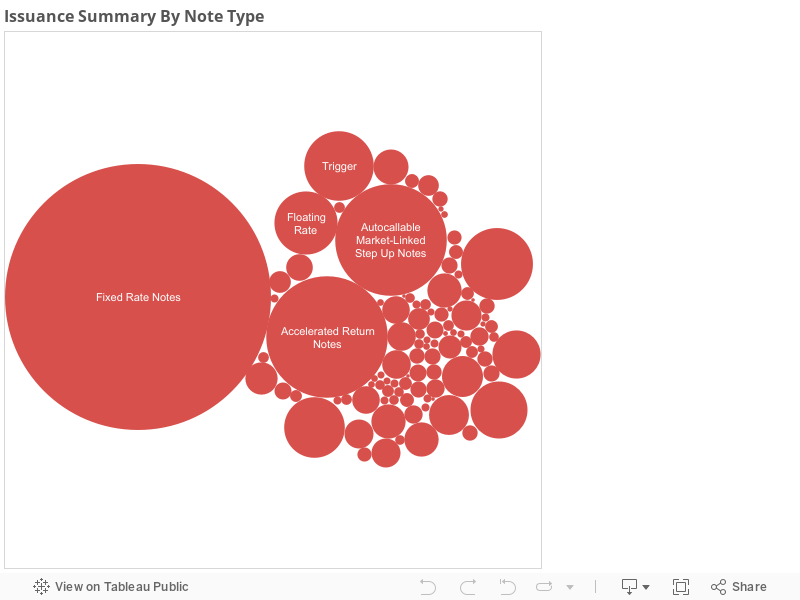

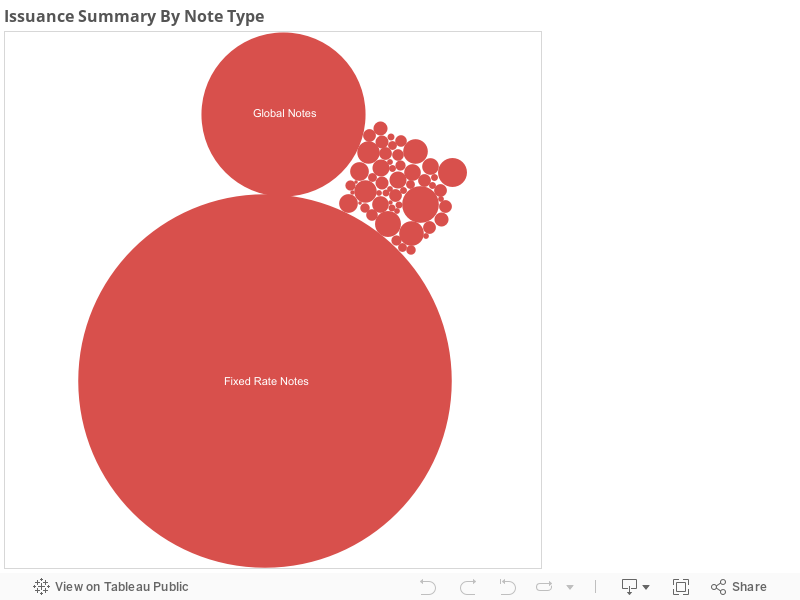

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Interest rate linked issuance limited to standard, step up callable notes and Fixed rate notes. Activity has been subdued this week.Citigroup, Wells Fargo are major issuers of these products. AT&T has issued CAD 1 Bn Fixed rate Note to the investors.Interestingly this note is one of the largest notes issued to the investors.

This week we have seen commodity note issuance tied to WTI crude oil. There has been a Currency linked note tied to USDMXN peso us issued by Goldman.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been interest rate linked notes.

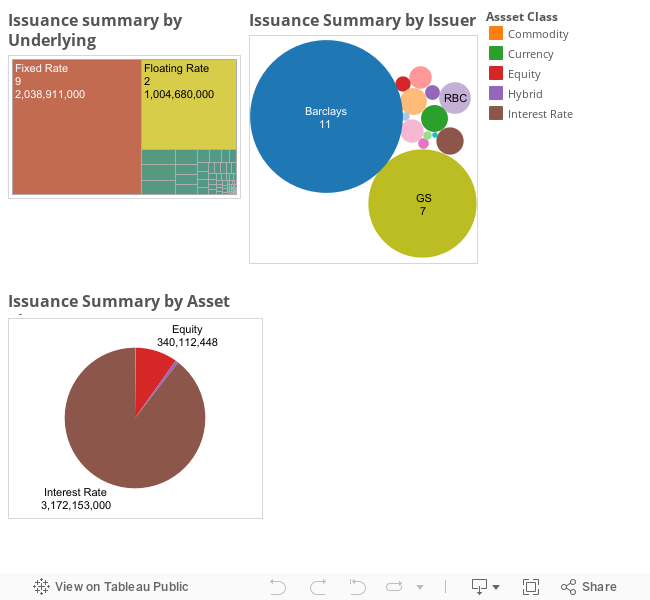

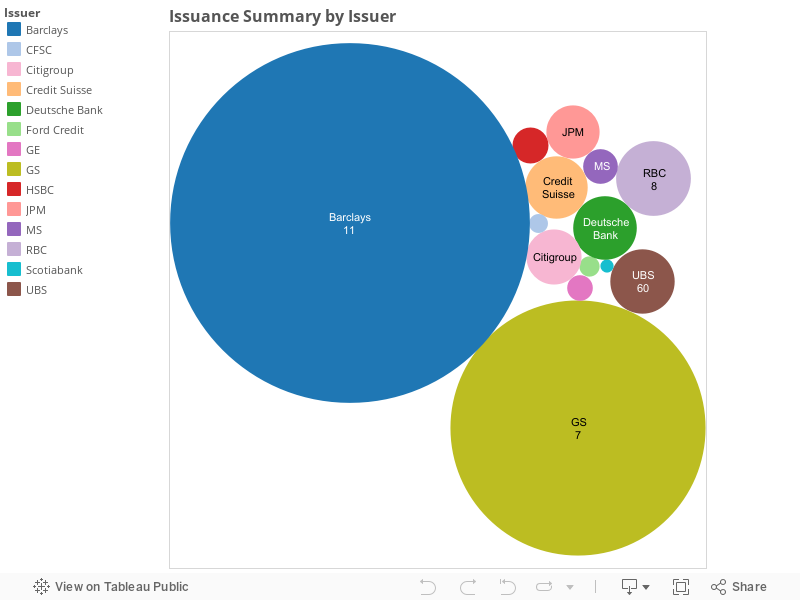

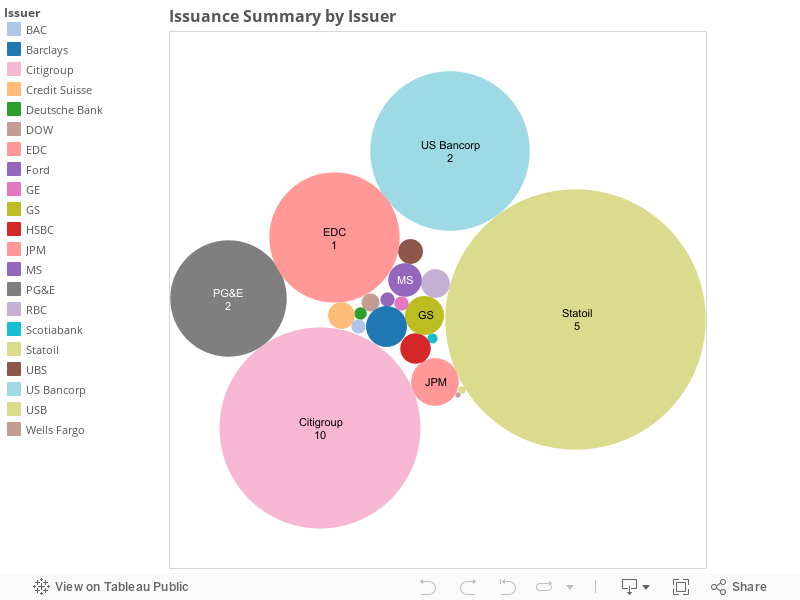

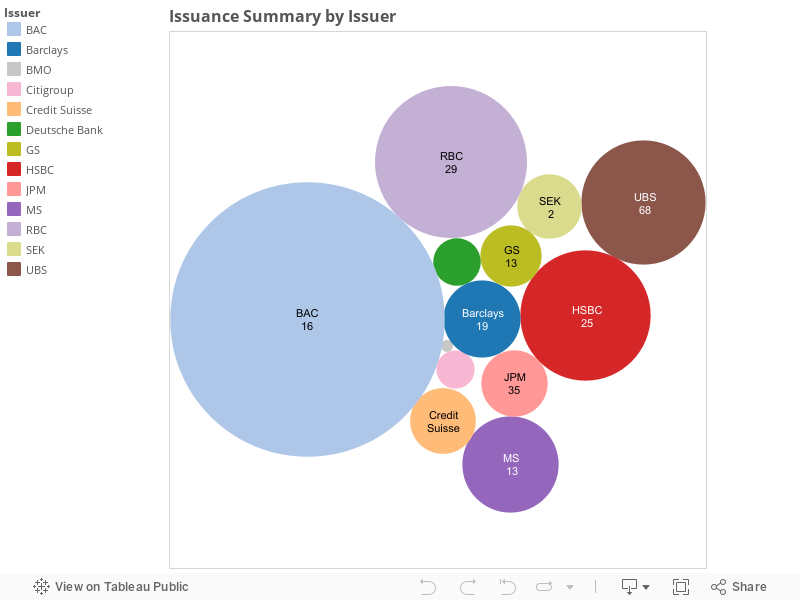

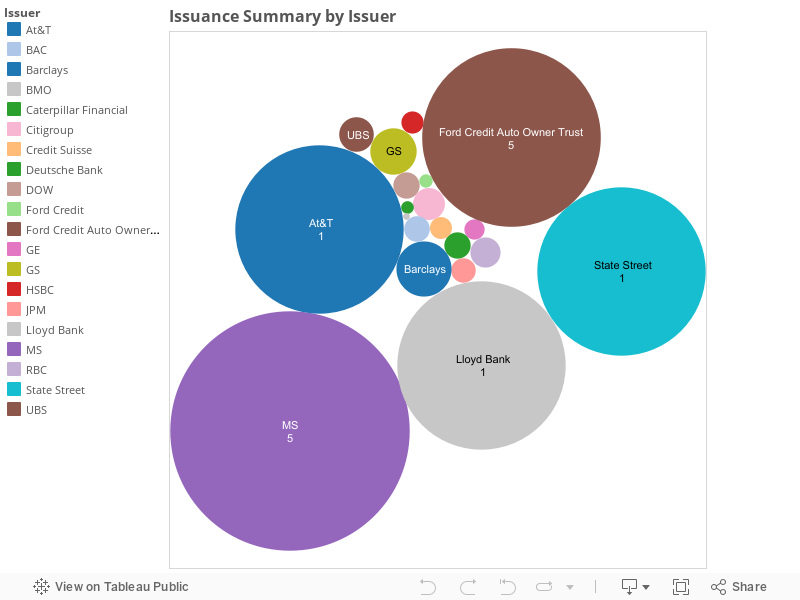

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week UBS, MS, GS and Barclays captured issuance market share.

Popular notes have been interest rate linked notes.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week UBS, MS, GS and Barclays captured issuance market share.

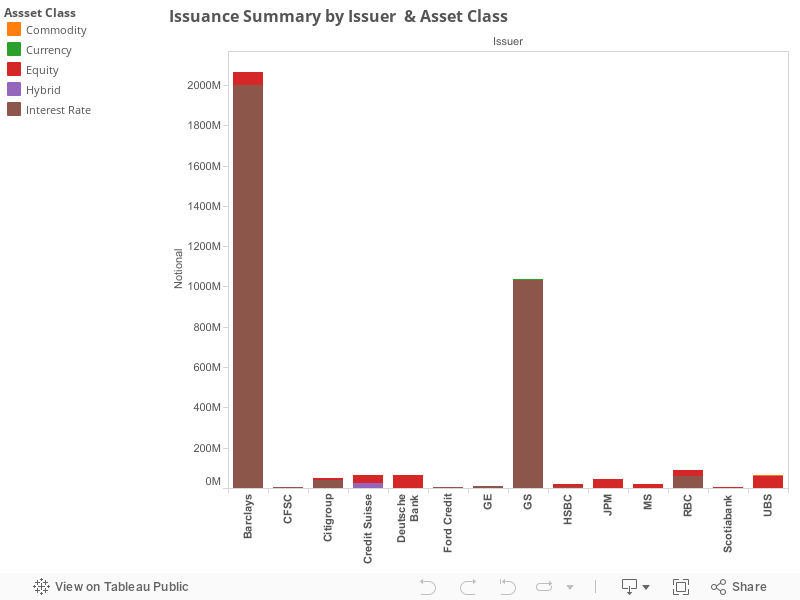

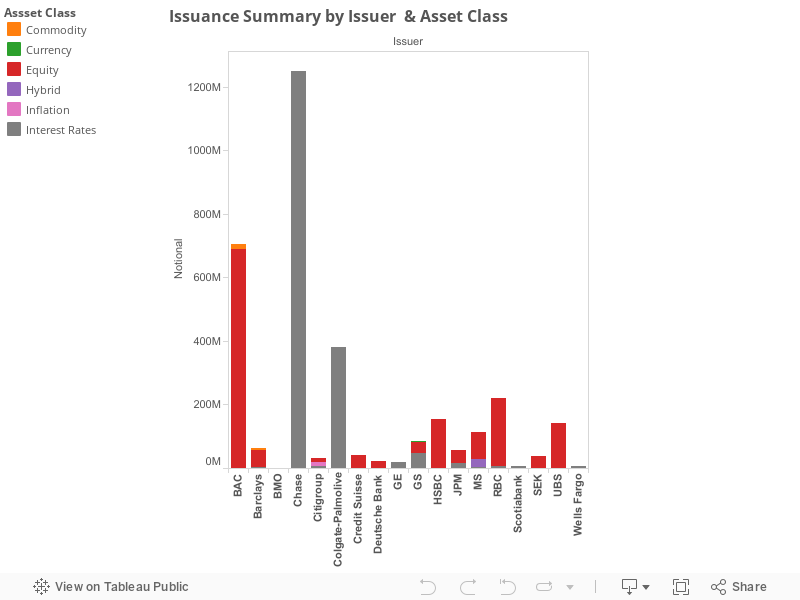

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.