Recently Exceed Investments found after surveying 700 financial advisors that structural inefficiencies like, Illiquidity and transparency are holding back the latent demand for structured investors. “Exceed Investments is a New York-based financial services firm developing next-generation structured investments. The firm commissioned a third party to conduct studies on structured investment perceptions in both 2013 and 2014, culminating in the proprietary 2014 Exceed Structured Investments Report. The goal of the research was to identify overall advisor views on and usage of structured products, with an eye towards identifying which steps the industry can take to increase utilization and acceptance.”

Research methodology • Research leadership – WealthManagement.com, a Penton Media company • Participants – 707 completed advisor surveys • Participant selection – Members of the Wealthmanagement.com database; random selection • Motivation – Participation led to eligibility in a lottery for several American Express gift cards

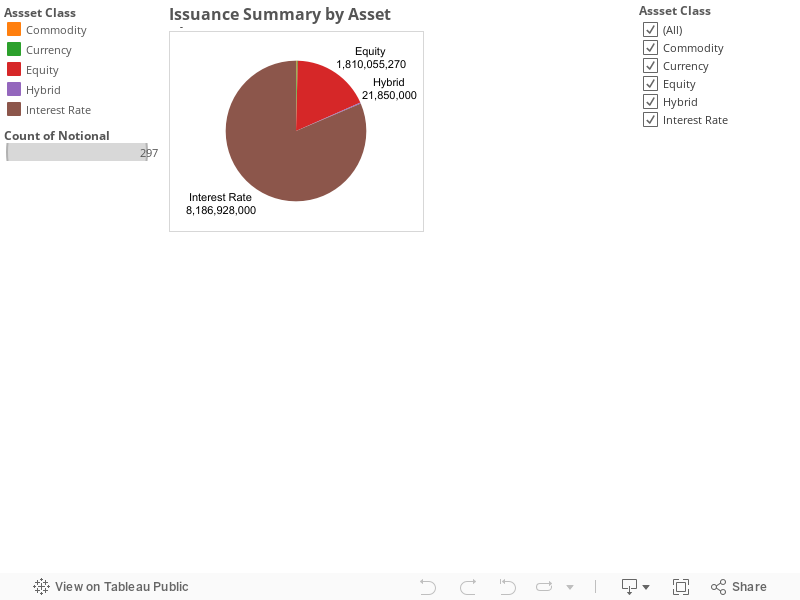

Why do we use structured notes?

Today investing world is replete with variety of investment options including derivative products. Commonly asked question is if I need exposure to a particular asset I can invest in that asset directly by buying a stock, or mutual fund or an ETF. Even I can create such a product sometimes using Options on those assets. All of these are true to certain extent. But like the name structured notes provide customized risk and reward profiles.

For instance, Yesterday I was discussing with a friend of mine about a Reverse Convetible note issued by a large bank is good investment or not. He immediately fired back, what is the return on the note. I told him 6% per annum for 6 years in this low interest environment. Compare this to US Treasuries that offer mere 2%. Next question came to me what is my risk. To this I said, if the index underlying Reverse Convertible goes below 50% of the initial index level on the maturity date you will lose corresponding capital otherwise you will get full return of capital. Now this kind of note can be deployed by understanding the Risk/reward metrics both historically and in probable future scenarios.

Below survey of Advisors speaks exactly to this fact that people want to use structured notes by understanding the Risk and Reward of these products.

Next question comes to mind is okay, you need structured notes but what features are most desirable. During my same discussion about the structured investments yesterday, another friend told me people are afraid of repeat of 2008 scenario. That is they want protection from secular decline in the market. This has been captured clearly by the Exceed investments survey on desirable features below. Most of the investors are looking for capital protection.

Alright, we know now some of the motivations behind the need for a structured investment. Then are these products being used more often or less often? Not surprisingly they are being use less as per survey below and my informal conversations. Most investors who lost their money investing in these products have considered moving away from them and some other have not understood these products so they do not have any interest.

We see in this chart, that structured notes are being used in very small portions despite their benefits. I guess this is so because of limited information about these products.

Now that we have looked at why structured notes are preferred and still not part of the overall portfolios. Let us take a look at some drivers for avoiding these products. Below survey speaks loud and clear these products are too complicated to understand and they tend to be highly illiquid. On the point of being too complicated I agree to some extent only. I agree products with strange names like Air Bag auto callable, Trigger phoenix autocallables, high low range accrual etc might confound an ordinary investor. I would think for an investor who is adept at handling latest mobile phone gadgets and navigating through them in 21st century spending some time to understand these products is time well spent. On the point of illiquidity, I think more people start holding these products market will start building its own secondary market.

I am a strong advocate of transparency around, the information on the structured note issuance, their market values and understanding of the underlying derivatives. Now as more and more people start understanding these products and associated risks and rewards we think market will improve. As you are witnessing in the Over the Counter derivatives markets, after moving the transactions to Swap exchange facilities and cleared space we are seeing spreads becoming narrower. This is natural consequence of the opening up markets. One important thing I found interesting in the survey is to reduce the minimum size. Now many issuers are currently coming up with products with small unit sizes.

Another important facet in the structured note business is distribution channel. Most of the distribution is being conducted via Wirehouses

If you are provided access to these structured products so that you can possibly help your investing clients benefit from these products. Most of them are still in the state of confusion rather than jump onto investing in the structured notes. This clearly indicates, Access to markets, understanding of the markets are both required to fully realize benefits of this market

I am actively advocating for transparency in the structured note markets through products like, Structured note database to what is on the market, Independent pricing to discover the market values and training and education to understand these markets better.

I am actively advocating for transparency in the structured note markets through products like, Structured note database to what is on the market, Independent pricing to discover the market values and training and education to understand these markets better.