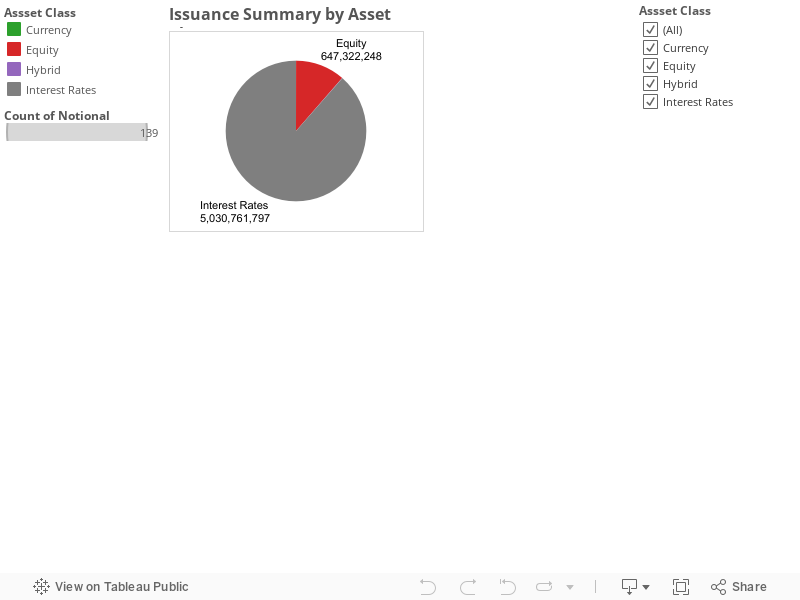

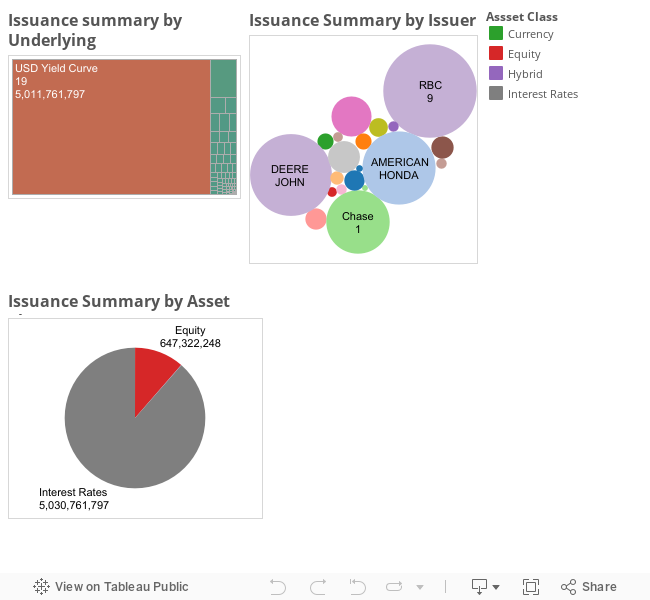

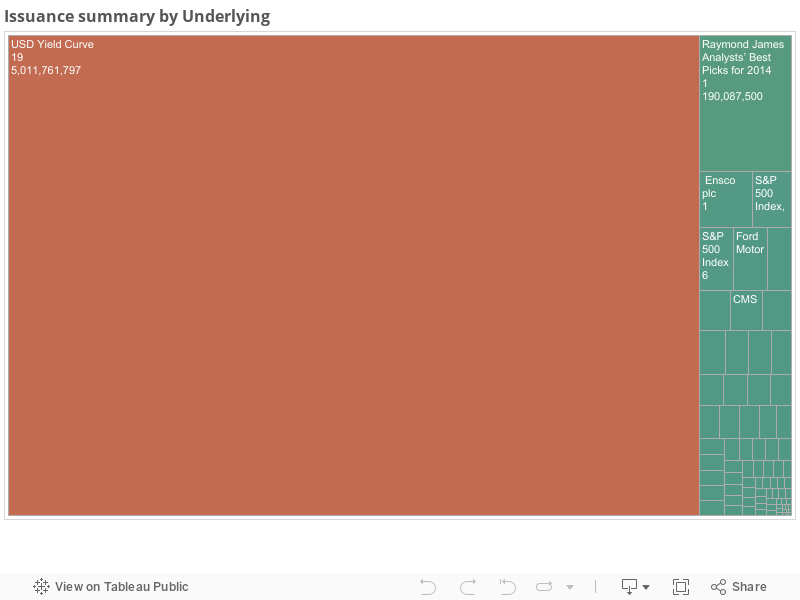

Performance Notes – Raymond James Analysts’ Best

Picks® for 2014 priced on December 10, 2013 by Bank of

Montreal

Equity Markets have been

rising for last two years and have reached post crisis highs. This performance

is filtered into underlying stocks like Apple, JPM, Comcast and other. BMO has

created a basket note tied to 13 different stocks that have been picked and

considered to be part of Raymond James Analyst's best pick of 2014. This note

has been deconstructed into its components to understand the mechanics of risk

and reward for this note.

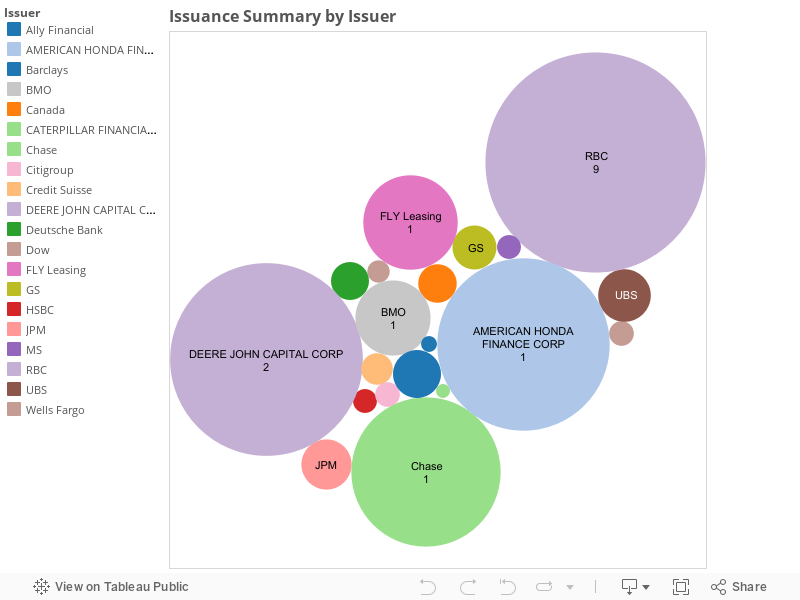

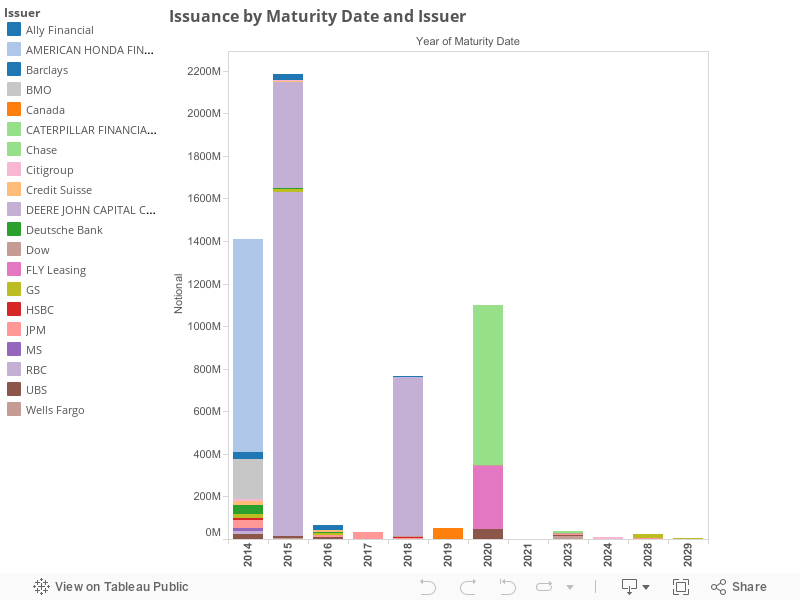

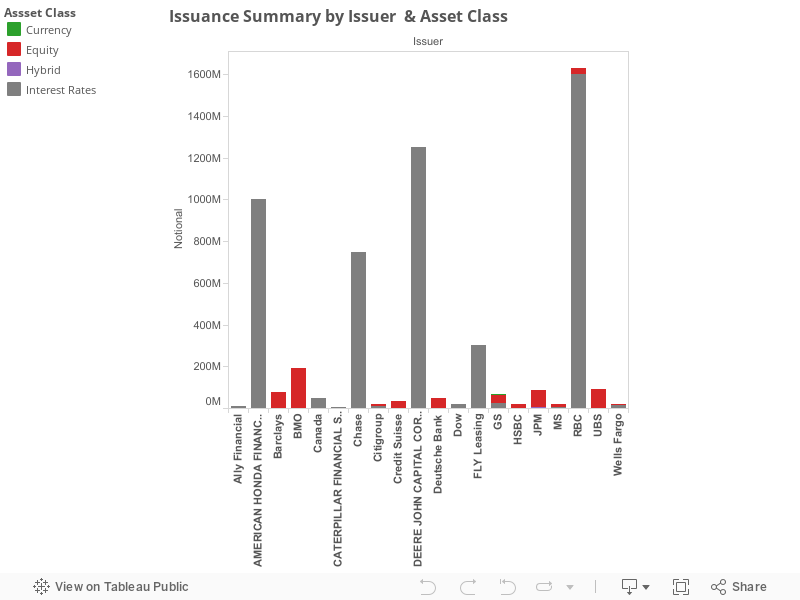

This performance Note

was priced by BMO for $1000.00 totaling a public offering of $185 million on

the basket of 13 stocks with a maturity on December 19, 2014. The Basket is composed of 13 Reference Shares, which

are the securities included in Raymond James Analysts’ Best Picks for 2014. These 13 names belong to different sectors of

the economy.

|

Advance

Auto Parts, Inc

|

Copa

Holdings, S.A.

|

Praxair,

Inc.

|

|

Antero

Resources Corporation

|

Ctrip.com

International, Ltd.

|

Quintiles

Transnational Holdings, Inc.

|

|

Apple

Inc.

|

Intuit

Inc.

|

Salesforce.com,

Inc.

|

|

Cameron

International Corporation

|

JPMorgan

Chase & Co.

|

Newell Rubbermaid Inc

|

|

Comcast

Corp.

|

||

The advantage of

this note is the 1-to-1 upside exposure to a basket of 13 stocks. Meaning each

percentage moves up would result in a one percent increase in returns. The

downside is the 1-to-1 downside exposure the return has should these 13 stocks

fall in price. In this note, Investors need not worry about missing dividends

like other structured notes as they are paid at the maturity. Investor is

primarily receiving a diversification into 13 stocks to attain above market

performance.

To replicate the note

investors would need to need to long a basket call with a strike at $100. This

should accelerate the returns 1-to-1. Main consideration for this basket option

would be correlation among 13 stock returns. Investor is capturing this

correlated performance through this note. On the down side, short a basket put

option with a strike at 100.

The credit risk for this

note is based on Bank of Montreal’s credit. The market risk is a reflection of underlying

13 single stock names performance. Here volatility of these stocks and

correlation among then is very important.

|

Ending

Basket Value

|

Redemption

Amount per Unit

|

Total

Rate of Return on the Notes

|

|

$60.00

|

$597.50

|

-41.85%

|

|

$70.00

|

$697.50

|

-32.12%

|

|

$80.00

|

$797.50

|

-22.38%

|

|

$90.00

|

$897.50

|

-12.65%

|

|

$100.00

|

$997.50

|

-2.92%

|

|

$103.00

|

$1027.50

|

-

|

|

$105.00

|

$1097.50

|

6.81%

|

|

$120.00

|

$1197.50

|

16.55%

|

|

$130.00

|

$1297.50

|

26.28%

|

|

$140.00

|

$1397.50

|

36.01%

|