During the week of August 19-23, 2013 structured note issuance has been 900 MM across various issuers and asset classes. Most of the issuance (87%) is driven by Equity linked notes and 7% of the issuance is driven by Interest rate linked products. For Details of the distribution refer to the chart below. Not surprisingly majority of the structured note issuance is linked to Equity linked.

Underlying analysis

Underlying analysis

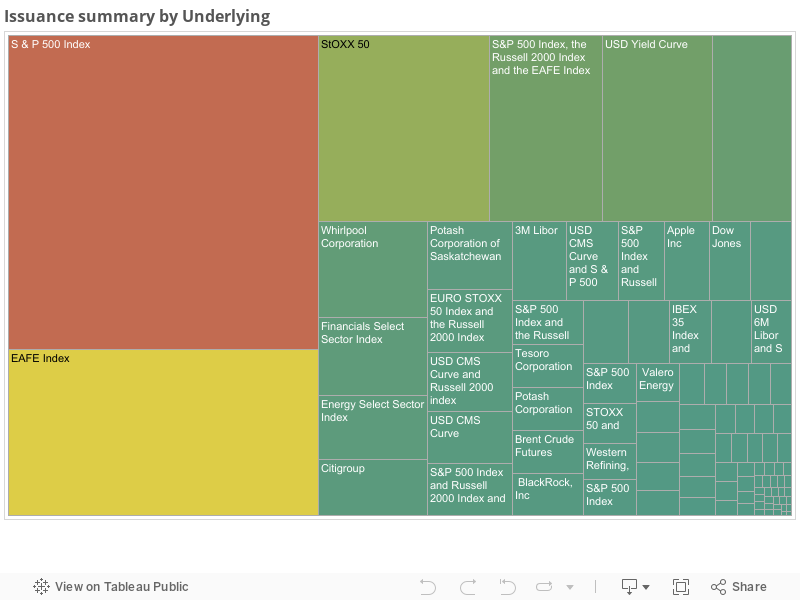

Issuers have been designing equity linked notes with variety of indices. Issuance related S&P 500, MSCI EAFE index and STOXX 50 Index have been close 50% of entire issuance. This shows how recent run up in the equity market has generated interest with in the market players. These 3 indices capture market performance in US, Developed markets outside North America and Euro region respectively. Bullish performance in developed equity markets contrasts the under performance in emerging markets that are plagued by falling currencies ( Brazil and India) and political turmoil (Egypt).

Notably Credit Suisse issued a large note on MSCI EAFE index to the investors. These notes belong to class of leveraged notes. They command twice the market performance capped at 16% coupon in this low yield environment. On the downside this note is protected loses up to 10% fall in the index. Beyond 10% fall in the index investors will participate in 1 to 1 downside. There is a possibility of losing 90% of the principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

Issuers have been designing equity linked notes with variety of indices. Issuance related S&P 500, MSCI EAFE index and STOXX 50 Index have been close 50% of entire issuance. This shows how recent run up in the equity market has generated interest with in the market players. These 3 indices capture market performance in US, Developed markets outside North America and Euro region respectively. Bullish performance in developed equity markets contrasts the under performance in emerging markets that are plagued by falling currencies ( Brazil and India) and political turmoil (Egypt).

Notably Credit Suisse issued a large note on MSCI EAFE index to the investors. These notes belong to class of leveraged notes. They command twice the market performance capped at 16% coupon in this low yield environment. On the downside this note is protected loses up to 10% fall in the index. Beyond 10% fall in the index investors will participate in 1 to 1 downside. There is a possibility of losing 90% of the principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

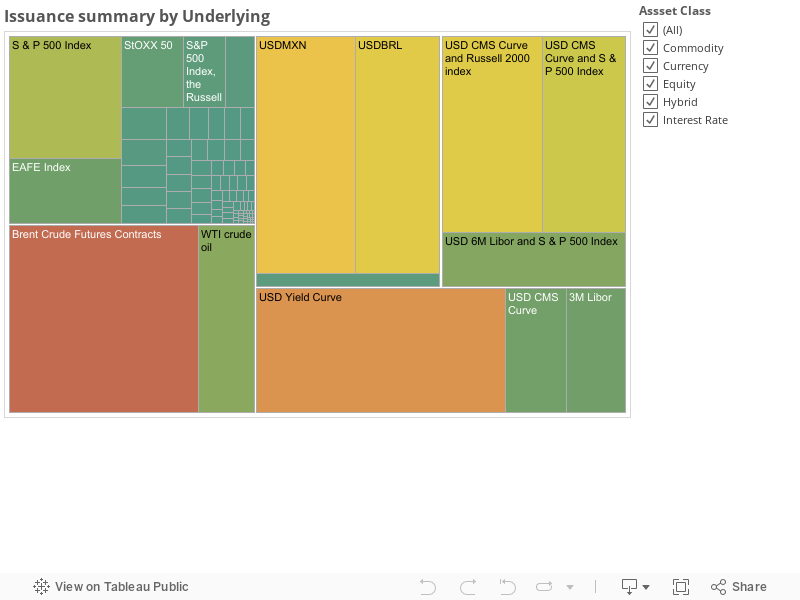

Interestingly With in Interest rate asset class some action is happening. There has been a surge in issuance of products linked Yield curve movements. For instance, JP Morgan has issued a note whose coupon tracks the performance of USD 6M Libor and S&P 500 Index joint performance. These notes pay a Coupon of 7.45% per year interest as long as interest rate 6M libor is below 6% and S&P 500 index is above 1250. For investors who have allocation in their bond component to attain better returns this note is a good deal. This Note is principal protected.

This fact can be attributed to Bernanke's response to QE related bond purchase tapering action and consequent impact on the yield curve. In general forward curve (a view on future Yield curve from Today;s spot curve) tells how much interest rates are going to rise and fall in the future. Investors can bet on this forward curve by purchasing notes whose performance is tied to CMS rates or yield curve. Some sophisticated investors take a position on the joint performance of the Interest rates and Equity market ( like Russell 2000) index.

There has been some issuance activity in Commodity and Currency segments of the markets. Currency asset class issuance have been tied to USDMXN, USDBRL and USDPLN currencies. These notes provide investors good returns as long as currencies settles does not depreciate more than 20%. Recently BRL currency has seen drop in its currency. This has prompted country central bank to execute swaps to protect from further drop in currency value. Investors can at least get a piece of this action.

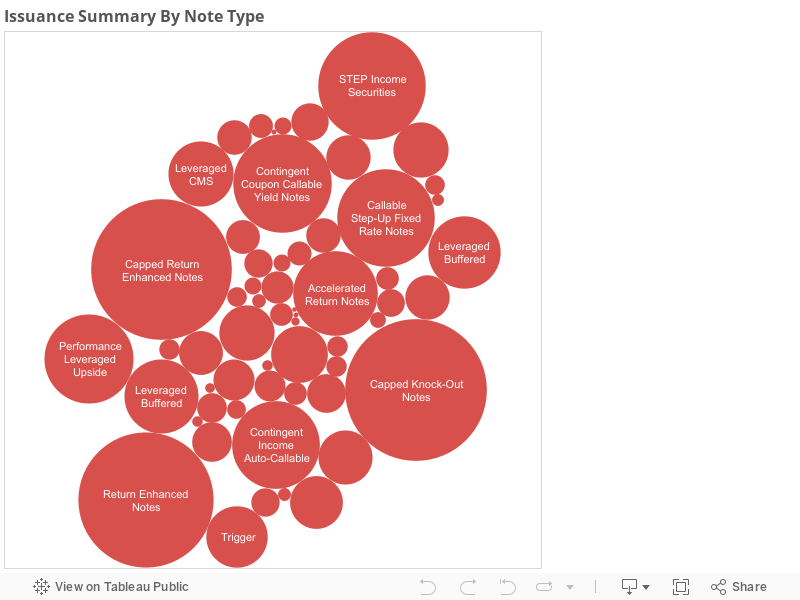

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Interestingly With in Interest rate asset class some action is happening. There has been a surge in issuance of products linked Yield curve movements. For instance, JP Morgan has issued a note whose coupon tracks the performance of USD 6M Libor and S&P 500 Index joint performance. These notes pay a Coupon of 7.45% per year interest as long as interest rate 6M libor is below 6% and S&P 500 index is above 1250. For investors who have allocation in their bond component to attain better returns this note is a good deal. This Note is principal protected.

This fact can be attributed to Bernanke's response to QE related bond purchase tapering action and consequent impact on the yield curve. In general forward curve (a view on future Yield curve from Today;s spot curve) tells how much interest rates are going to rise and fall in the future. Investors can bet on this forward curve by purchasing notes whose performance is tied to CMS rates or yield curve. Some sophisticated investors take a position on the joint performance of the Interest rates and Equity market ( like Russell 2000) index.

There has been some issuance activity in Commodity and Currency segments of the markets. Currency asset class issuance have been tied to USDMXN, USDBRL and USDPLN currencies. These notes provide investors good returns as long as currencies settles does not depreciate more than 20%. Recently BRL currency has seen drop in its currency. This has prompted country central bank to execute swaps to protect from further drop in currency value. Investors can at least get a piece of this action.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been capped Knockout notes, capped return enhanced notes and return enhanced notes. All three notes are equity index related notes designed to capture the leveraged performance in the equity markets. This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will not be posting double digit returns.

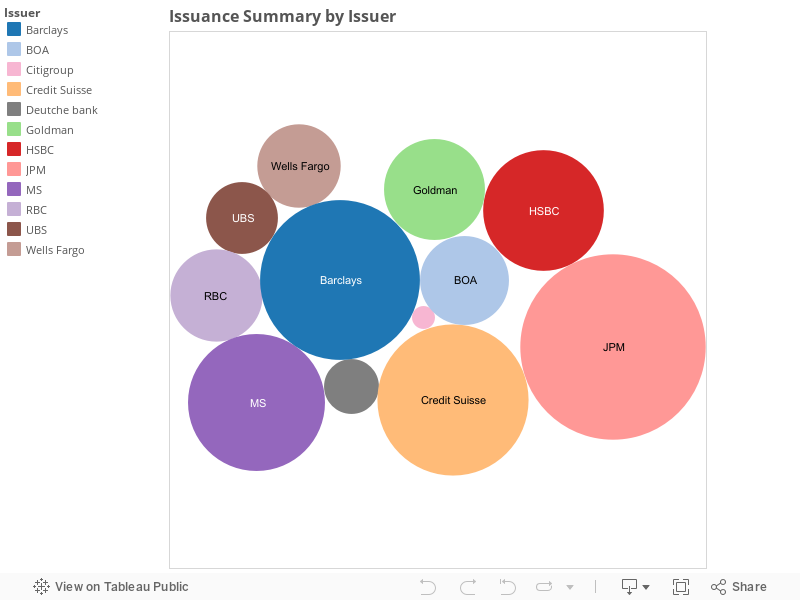

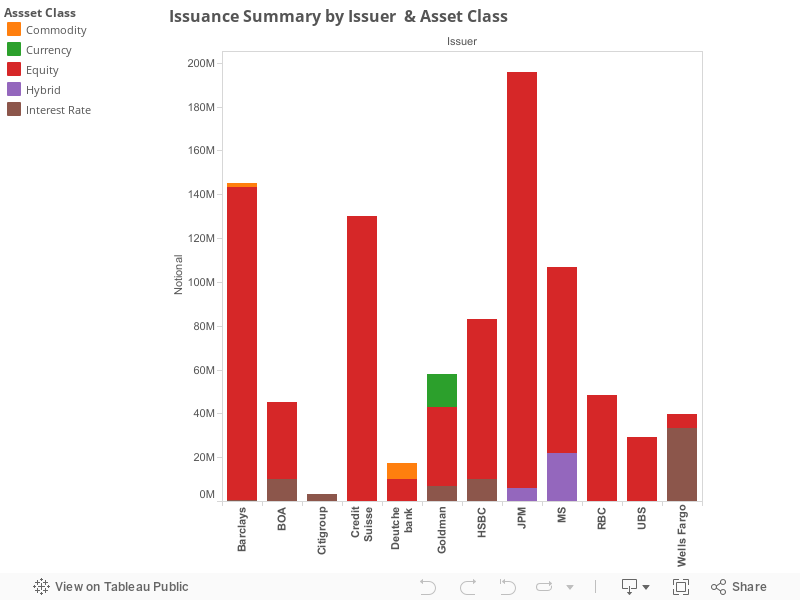

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week JP Morgan with its large issuances of Equity linked notes captured 22% of the issuance volume. Barclays, Morgan Stanley and Credit Suisse captured market share near mid 20s and high 10s.

Popular notes have been capped Knockout notes, capped return enhanced notes and return enhanced notes. All three notes are equity index related notes designed to capture the leveraged performance in the equity markets. This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will not be posting double digit returns.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week JP Morgan with its large issuances of Equity linked notes captured 22% of the issuance volume. Barclays, Morgan Stanley and Credit Suisse captured market share near mid 20s and high 10s.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

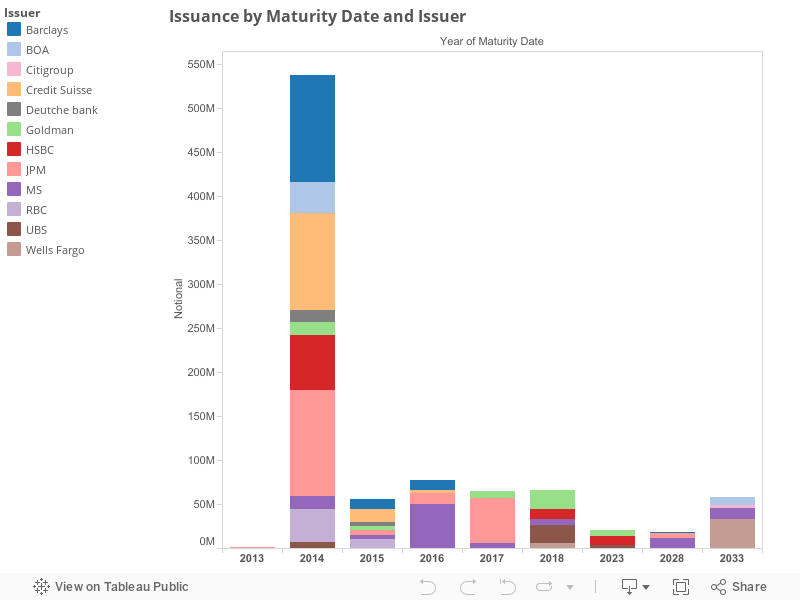

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume matures in 2014. This can be attributed to two facts. Notes maturing in 2014 are mostly equity linked notes.

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume matures in 2014. This can be attributed to two facts. Notes maturing in 2014 are mostly equity linked notes.

For additional details please refer to the Issuance summary table.

For additional details please refer to the Issuance summary table.

No comments:

Post a Comment