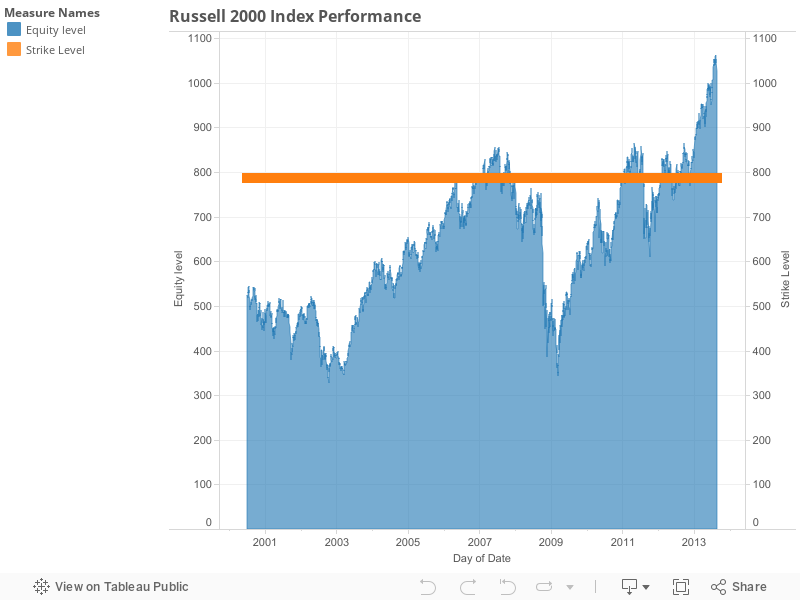

Equity markets have posted double digit returns so far. Russell 2000 index has risen by 22% year to date showing that economy has improved from the significant lows of 2009. Bond market yields started to rise and US Federal Reserve started slowing its famous quantitative easing related buying. This is giving investors opportunities to participate in rising yield curve environment and bullish equity market simultaneously. This theme can be captured in variety of ways. One of them would be investing in a Leveraged CMS curve and Russell 2000 index linked note issued by Morgan Stanley with Cusip: 61760QDA9. This note pays a quarterly coupon of 10% in year 1. After that for each day Russell 2000 index is above 785.85 it will pay 4 times the difference between USD CMS30Y Rate and USD CMS2Y Rate determined at the start of the quarter capped at 10% and floored at 0%.

Some pros and cons to be considered before doing a deep dive into this investment

Pros

1) 10% coupon in the first year

2) Possibility of participating in steepening of yield curve with 4 times leverage and obtaining 10% coupon

3) Floor at zero protects loss of initial capital.

Cons:

1) Principal is exposed to Morgan Stanley credit risk

2) Russell 2000 has been above 785.85 for last 2 years only in last 12 years. So there might be chance of interest not accruing on certain periods.

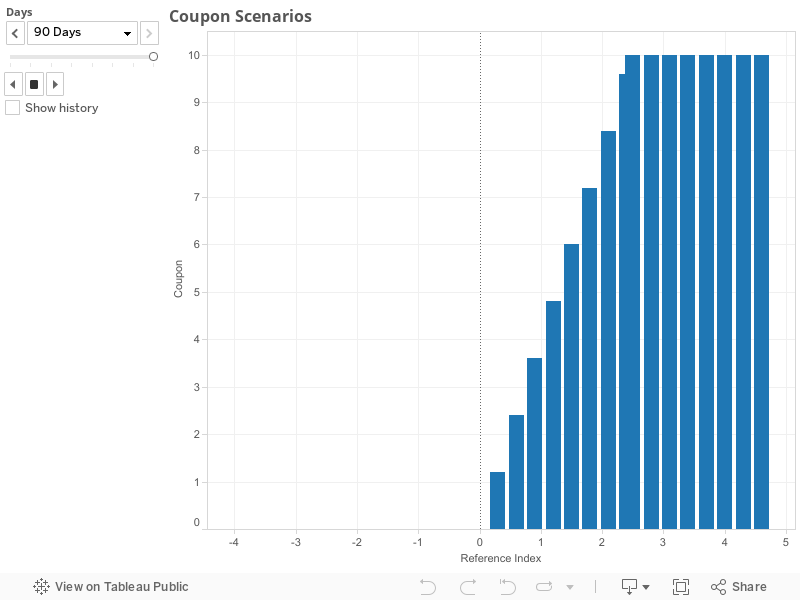

Coupon Scenarios:

Investors can visualize the amount of coupon they can receive for different number of accrual days when Russell 2000 index is above the strike level of 785.85 and level of CMS30y-CMS2y spread. This gives clear understanding of leverage involved in the product and joint performance of the curve steepening and Russell index being above the strike level. Magnitude of coupon is function of number of day Russell 2000 is above the strike level and steepness of the yield curve. There will be zero coupon if Russell 2000 is below the strike level or yield curve is inverted (Spread is negative).

Coupon Scenarios:

Investors can visualize the amount of coupon they can receive for different number of accrual days when Russell 2000 index is above the strike level of 785.85 and level of CMS30y-CMS2y spread. This gives clear understanding of leverage involved in the product and joint performance of the curve steepening and Russell index being above the strike level. Magnitude of coupon is function of number of day Russell 2000 is above the strike level and steepness of the yield curve. There will be zero coupon if Russell 2000 is below the strike level or yield curve is inverted (Spread is negative).

Risks

This product exposes investors to market risk arising from Equity markets (Russell 2000 index), Interest rates market (CMS30y-CMS2y), correlation between these two markets and finally to the credit risk from the issuer (Morgan Stanley).

These risks can be understood by looking at the components that are involved in constructing or replicating the payoff of this product

Payoff replication

This note payoff can be replicated by

1) Long 1 unit of Range Accrual option on Russell 2000 at 785.85 strike

2) Long 4 units of CMS 30y Swap

3) Short 4 units of CMS 2y Swap

4) Short 4 units of CMS30Y-CMS2y Spread Cap at strike 10%

5) Long 4 units of CMS30Y-CMS2y Spread floor at Zero Strike

6) Long 1 unit of 10% coupon 1y bond

7) Long 1 unit of correlation between Russell 2000 and CMS30y-CMS2y

These seven components together determine the value of the note at each point in time before the maturity of the note.

for detailed analysis on note and its components please feel to contact me.

Risks

This product exposes investors to market risk arising from Equity markets (Russell 2000 index), Interest rates market (CMS30y-CMS2y), correlation between these two markets and finally to the credit risk from the issuer (Morgan Stanley).

These risks can be understood by looking at the components that are involved in constructing or replicating the payoff of this product

Payoff replication

This note payoff can be replicated by

1) Long 1 unit of Range Accrual option on Russell 2000 at 785.85 strike

2) Long 4 units of CMS 30y Swap

3) Short 4 units of CMS 2y Swap

4) Short 4 units of CMS30Y-CMS2y Spread Cap at strike 10%

5) Long 4 units of CMS30Y-CMS2y Spread floor at Zero Strike

6) Long 1 unit of 10% coupon 1y bond

7) Long 1 unit of correlation between Russell 2000 and CMS30y-CMS2y

These seven components together determine the value of the note at each point in time before the maturity of the note.

for detailed analysis on note and its components please feel to contact me.

No comments:

Post a Comment