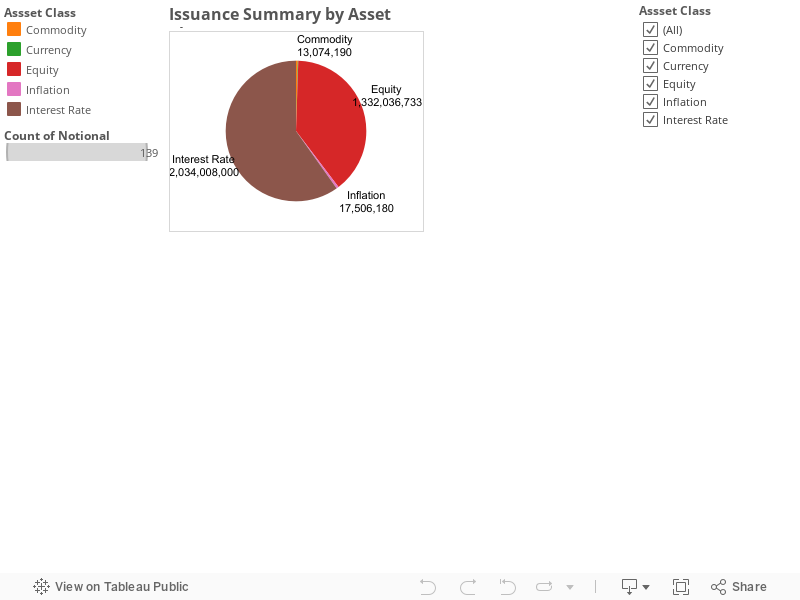

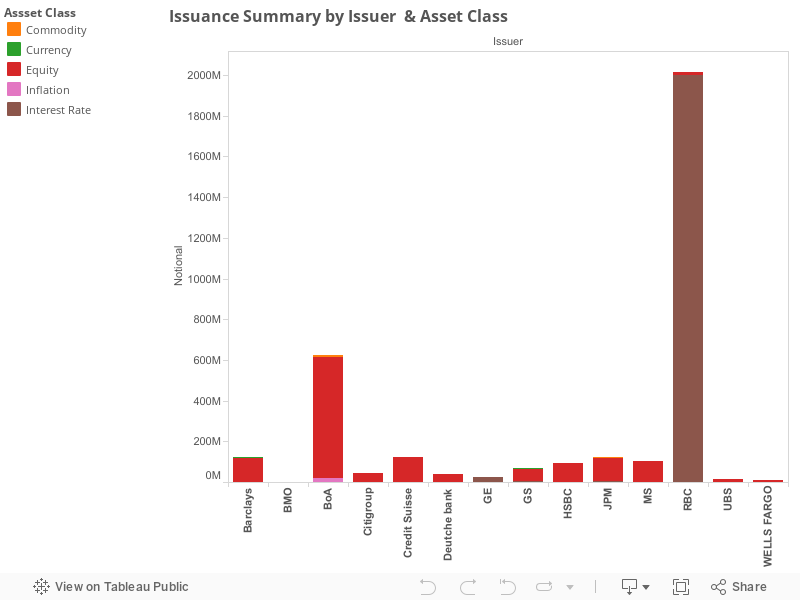

During the week of September 02-06, 2013 structured note issuance has been 3.4 BN across various issuers and asset classes. Most of the issuance (2 BN) is driven by Interest Rate linked notes and 1.3 BN of the issuance is driven by Equity linked products. For Details of the distribution refer to the chart below. Surprisingly majority of the structured note issuance is linked to Interest Rate linked.

Interactive Issuance analysis

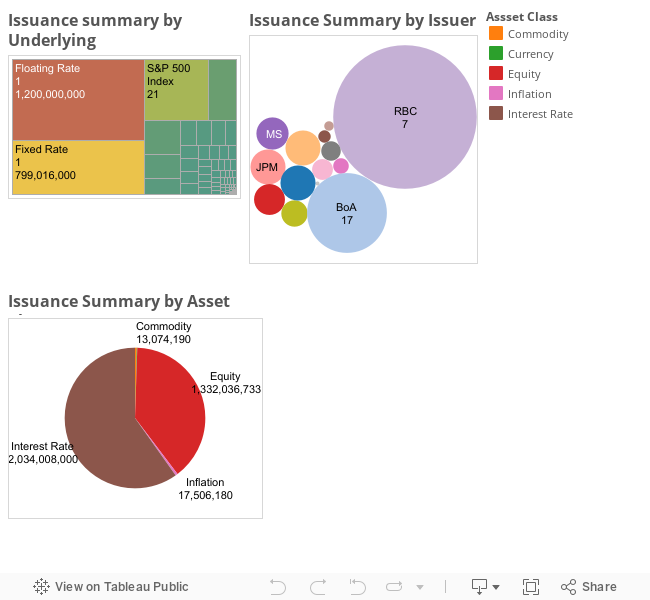

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

Interactive Issuance analysis

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

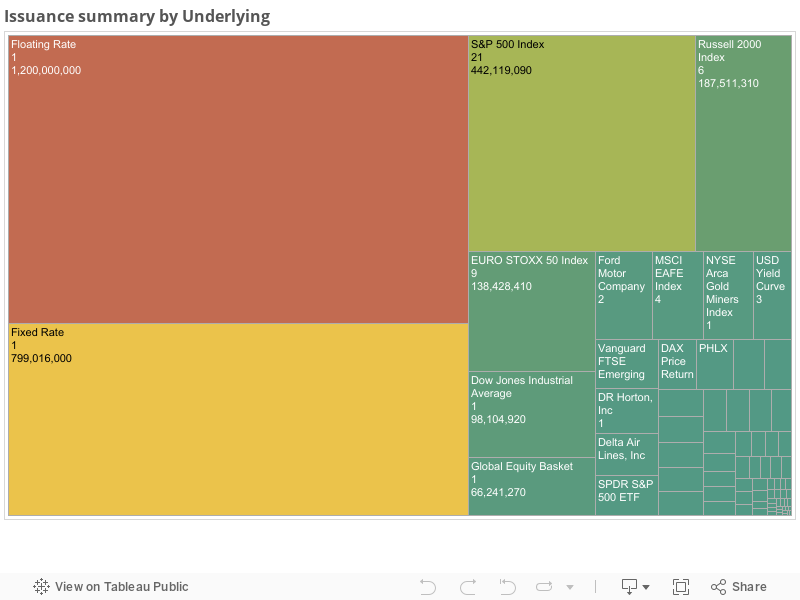

Underlying analysis

Underlying analysis

RBC has issued two large interest rate linked fixed and floating rate notes. These two notes mature in september 2016. 1.2 Billion Floating rates paying a coupon of 3M Libor+ 46 bps and suitable for investors seeking to tap into the rising interest rates. Another note with a notional of 800 MM with coupon of 1.45% paid semi annually for 3 years has been issued. This might not be a best deal for an aggressive investor but definitely better yields when compared to US Treasury 3Y yielding 89 bps this is note is better by 60 bps.

On the Equity linked notes front there has been good amount of activity. Bank of America leading the pack with 44 % market share.

Notably BOA issued a large note on Dow Jones Industrial Average index to the investors. These notes belong to class of leveraged notes. They command 1.256 times the market performance without any cap. On the downside this note is protected loses up to 75% fall in the index. Beyond 75% fall in the index investors will participate in 1 to 1 downside. There is a possibility of losing 75% of the principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

This Week BOA issued a note whose coupon tracks the performance of DAX Price return Index. These notes pay a Coupon of 21 % per year at maturity if the index is above initial level but below step level (21%). Beyond this step level, investor get market performance uncapped. On the down side, investor participates 1:1 market performance. This Note is not principal protected

There has been some issuance activity in Commodity and Currency segments of the markets. Currency asset class issuance have been tied to USDMXN currency. This note provide investors good returns as long as currencies settles does not depreciate more than 20%.

With in the Commodity space, Gold and OIL linked notes were made available to investors. Giving investors an opportunity to obtain accelerated returns on the underlying changes.

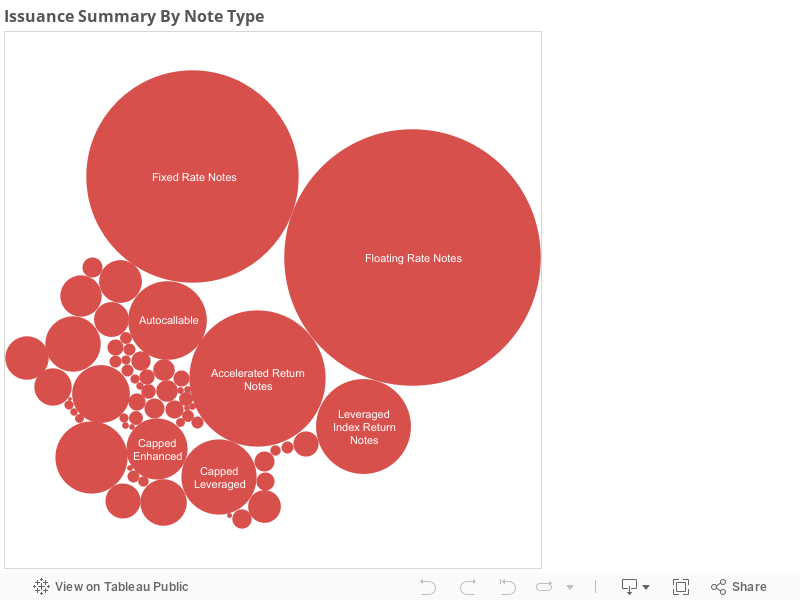

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

RBC has issued two large interest rate linked fixed and floating rate notes. These two notes mature in september 2016. 1.2 Billion Floating rates paying a coupon of 3M Libor+ 46 bps and suitable for investors seeking to tap into the rising interest rates. Another note with a notional of 800 MM with coupon of 1.45% paid semi annually for 3 years has been issued. This might not be a best deal for an aggressive investor but definitely better yields when compared to US Treasury 3Y yielding 89 bps this is note is better by 60 bps.

On the Equity linked notes front there has been good amount of activity. Bank of America leading the pack with 44 % market share.

Notably BOA issued a large note on Dow Jones Industrial Average index to the investors. These notes belong to class of leveraged notes. They command 1.256 times the market performance without any cap. On the downside this note is protected loses up to 75% fall in the index. Beyond 75% fall in the index investors will participate in 1 to 1 downside. There is a possibility of losing 75% of the principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

This Week BOA issued a note whose coupon tracks the performance of DAX Price return Index. These notes pay a Coupon of 21 % per year at maturity if the index is above initial level but below step level (21%). Beyond this step level, investor get market performance uncapped. On the down side, investor participates 1:1 market performance. This Note is not principal protected

There has been some issuance activity in Commodity and Currency segments of the markets. Currency asset class issuance have been tied to USDMXN currency. This note provide investors good returns as long as currencies settles does not depreciate more than 20%.

With in the Commodity space, Gold and OIL linked notes were made available to investors. Giving investors an opportunity to obtain accelerated returns on the underlying changes.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been Accelerated Notes, Fixed and Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. Accelerated return notes provide leveraged returns to investors and note have been issued using Equity indices like Dow jone (DJIA Index), S&P 500 (SPX Index) etc.

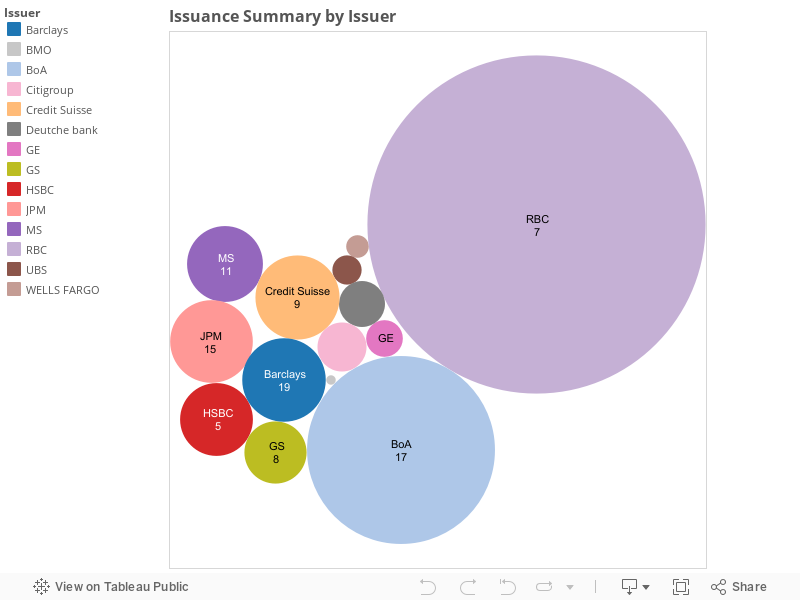

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week RBC with its large issuances of Interest Rate linked notes captured 60% of the issuance volume. BoA, JPM, HSBC and MS captured market share around 3%.

Popular notes have been Accelerated Notes, Fixed and Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. Accelerated return notes provide leveraged returns to investors and note have been issued using Equity indices like Dow jone (DJIA Index), S&P 500 (SPX Index) etc.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week RBC with its large issuances of Interest Rate linked notes captured 60% of the issuance volume. BoA, JPM, HSBC and MS captured market share around 3%.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

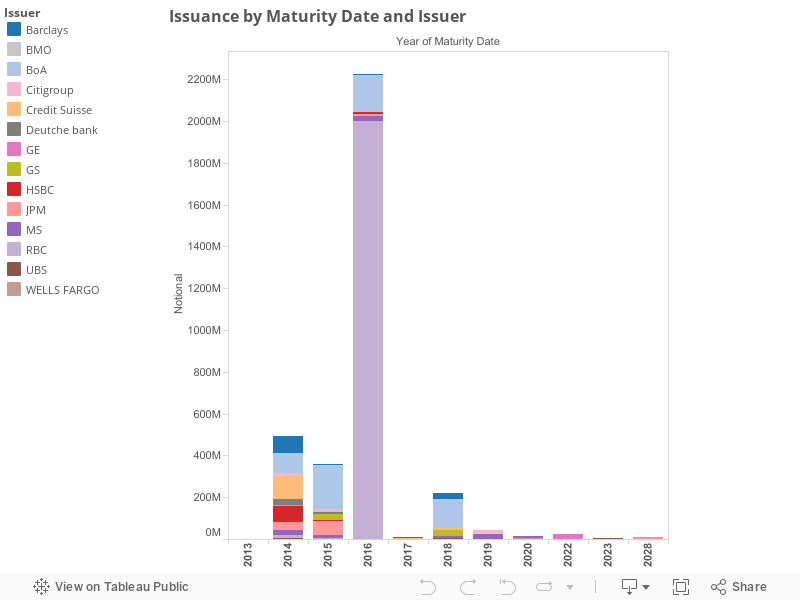

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2016. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2016. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

For additional details please refer to the Issuance summary table.

For additional details please refer to the Issuance summary table.

No comments:

Post a Comment