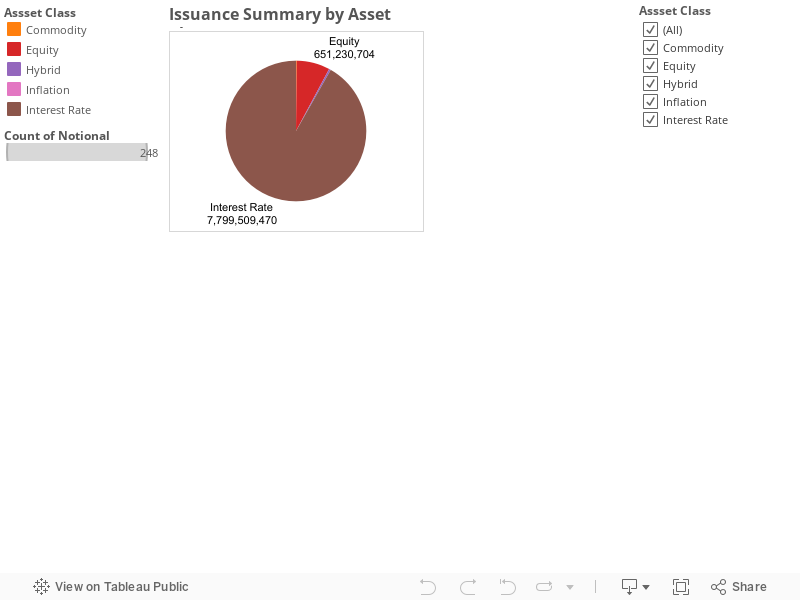

During the week of September 23-27, 2013 structured note issuance has been 8.4 BN across various issuers and asset classes. Most of the issuance (7.7 BN) is driven by Interest Rate linked notes and 650 MM of the issuance is driven by Equity linked products. Interestingly Hybrid linked issuance has spiked this week. For Details of the distribution refer to the chart below. Surprisingly majority of the structured note issuance is linked to Interest Rate linked.

This week, structured notes were issued with variety of flavors and interesting themes. Some of them include Global bond by Mexico government, Interest rate-Foreign Exchange linked hybrid note from Deutche bank to monetize their view on USD-JPY Exchange rate versus USD 5y Swap rate. Read on for more details.

Interactive Issuance analysis

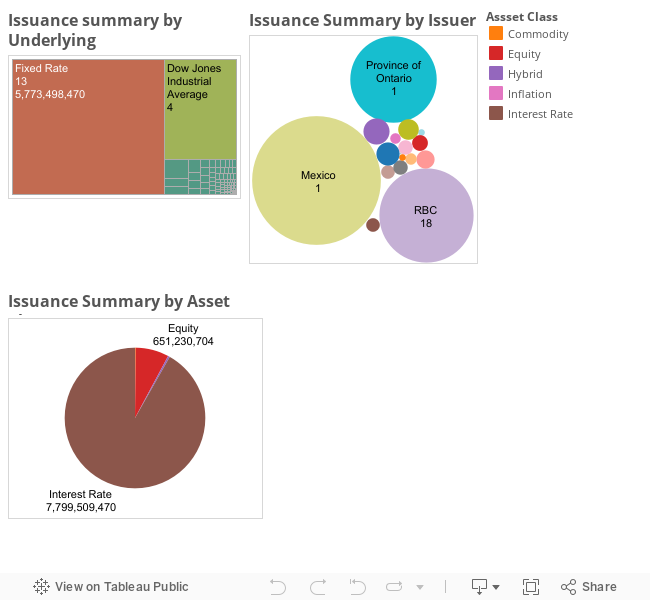

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

Interactive Issuance analysis

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

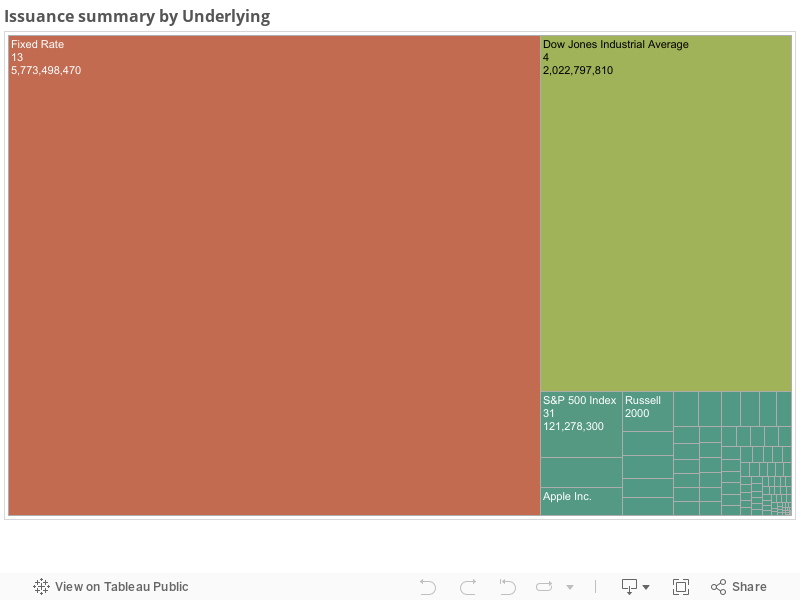

Underlying analysis

Underlying analysis

Mexico has issued one large interest rate linked global notes. This note matures in September 2023. 3.8 Bn Fixed rates paying a coupon of 4 % and suitable for investors seeking to tap into the rising interest rates. This might be a good deal for an aggressive investor and definitely better yields when compared to US 10Y Treasury. These notes carry Mexico sovereign risk. In other words if Mexico miss on making payments investors risk losing their principal. Province of Ontario issued a 1.7 bn interest linked note to issuers. These notes mature in September 2018 paying 2 % coupon. This is a safe note that is exposed to credit risk of province of Ontario.

Mexico has issued one large interest rate linked global notes. This note matures in September 2023. 3.8 Bn Fixed rates paying a coupon of 4 % and suitable for investors seeking to tap into the rising interest rates. This might be a good deal for an aggressive investor and definitely better yields when compared to US 10Y Treasury. These notes carry Mexico sovereign risk. In other words if Mexico miss on making payments investors risk losing their principal. Province of Ontario issued a 1.7 bn interest linked note to issuers. These notes mature in September 2018 paying 2 % coupon. This is a safe note that is exposed to credit risk of province of Ontario.

On the Equity linked notes front there has been good amount of activity. Notes have been created on variety of underlyings. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Apple, CME, Emerging markets ETF, Pulte group, Linkedin) and JPM proprietary volatility index.

JPM has issued 6.4 MM note to the investors on J.P. Morgan Strategic Volatility Index to the investors maturing in 12/31/14.

The J.P. Morgan Strategic Volatility Index (the “Index”) is a synthetic, rules-based proprietary index developed and maintained by JPMS plc. The level of the Index is published each trading day under the Bloomberg ticker symbol “JPUSSTVL.” The Index was created on July 30, 2010, and therefore has limited historical performance.

Main features of the JPM Strategic Volatility index

1) Index is a dynamic replication strategy on CBOE Volatility Index ( VIX index)

2) Index position is akin to synthetically creating a position in VIX futures contract.

3) Index employs Long-Short strategy on the VIX Future contracts

4) Contango in VIX markets might lead to lower or negative returns. That is Future Contracts in latter months are higher than the spot contract.

5) This kind of return cannot be replicated by using Do it your self option strategy.

Investors who are sophisticated enough to understand the nuances of the VIX market should buy this note.

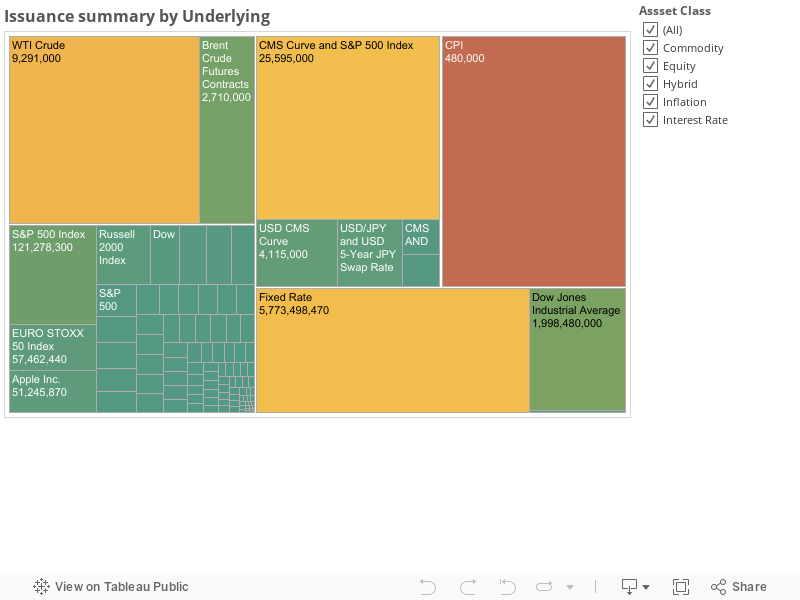

There has been some issuance activity in Commodity and Currency segments of the markets.

Notable note issued by Barclays to capture performance of Brent crude oil. I guess Middle East geopolitics play can be captured into your portfolio by entering into this contract. Barclays issued 103 MM worth of Brent crude oil based yield enhancement class structured note. These notes command a maximum of 15% if Brent crude oil rises and will participate 1:1 downside performance with risk of losing entire principal.

On the Hybrid segment side, this week Morgan Stanley has issued some CMS and S&P 500 index linked notes. Interestingly, Deutche bank issued a note linking USD-JPY currency and JPY 5y Swap rate performance. This note is designed to express a view on weakening JPY and Rising interest rates. This note pays investor Currency performance and Interest Rate performance as long as USD/JPY exchange rate is above 120 and swap rates rise above 2%. This deal expires in 2 years. If the investor view does not materialize, investor will be losing 40% of the principal. Potentially risk note but for a adventurous investor may provide additional gains to his portfolio.

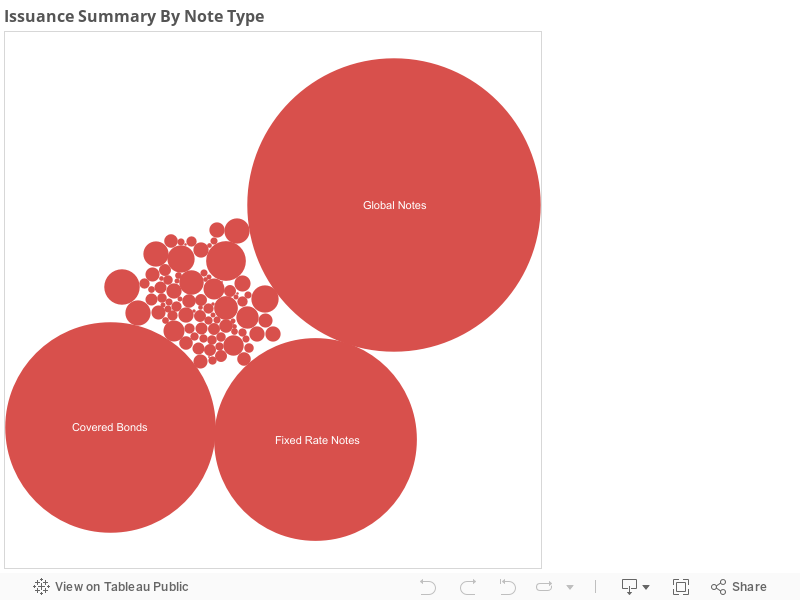

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

On the Equity linked notes front there has been good amount of activity. Notes have been created on variety of underlyings. This week issuance included notes created on the indices ( S&P 500, Stoxx 50, Russell 2000) and single names ( Apple, CME, Emerging markets ETF, Pulte group, Linkedin) and JPM proprietary volatility index.

JPM has issued 6.4 MM note to the investors on J.P. Morgan Strategic Volatility Index to the investors maturing in 12/31/14.

The J.P. Morgan Strategic Volatility Index (the “Index”) is a synthetic, rules-based proprietary index developed and maintained by JPMS plc. The level of the Index is published each trading day under the Bloomberg ticker symbol “JPUSSTVL.” The Index was created on July 30, 2010, and therefore has limited historical performance.

Main features of the JPM Strategic Volatility index

1) Index is a dynamic replication strategy on CBOE Volatility Index ( VIX index)

2) Index position is akin to synthetically creating a position in VIX futures contract.

3) Index employs Long-Short strategy on the VIX Future contracts

4) Contango in VIX markets might lead to lower or negative returns. That is Future Contracts in latter months are higher than the spot contract.

5) This kind of return cannot be replicated by using Do it your self option strategy.

Investors who are sophisticated enough to understand the nuances of the VIX market should buy this note.

There has been some issuance activity in Commodity and Currency segments of the markets.

Notable note issued by Barclays to capture performance of Brent crude oil. I guess Middle East geopolitics play can be captured into your portfolio by entering into this contract. Barclays issued 103 MM worth of Brent crude oil based yield enhancement class structured note. These notes command a maximum of 15% if Brent crude oil rises and will participate 1:1 downside performance with risk of losing entire principal.

On the Hybrid segment side, this week Morgan Stanley has issued some CMS and S&P 500 index linked notes. Interestingly, Deutche bank issued a note linking USD-JPY currency and JPY 5y Swap rate performance. This note is designed to express a view on weakening JPY and Rising interest rates. This note pays investor Currency performance and Interest Rate performance as long as USD/JPY exchange rate is above 120 and swap rates rise above 2%. This deal expires in 2 years. If the investor view does not materialize, investor will be losing 40% of the principal. Potentially risk note but for a adventurous investor may provide additional gains to his portfolio.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been Fixed Rate Notes, Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. This week market activity has been shadowed by one large issuance by Mexico state and province of Ontario.

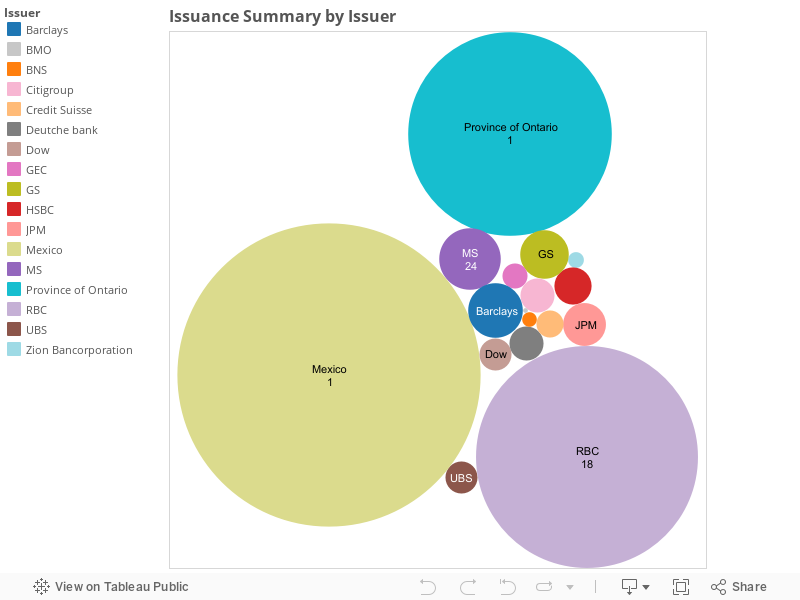

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week Mexico State and province of Ontario with its large issuances of Interest Rate linked notes captured 50% of the issuance volume. JPM, RBC and GS captured rest of the issuance market share.

Popular notes have been Fixed Rate Notes, Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. This week market activity has been shadowed by one large issuance by Mexico state and province of Ontario.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week Mexico State and province of Ontario with its large issuances of Interest Rate linked notes captured 50% of the issuance volume. JPM, RBC and GS captured rest of the issuance market share.

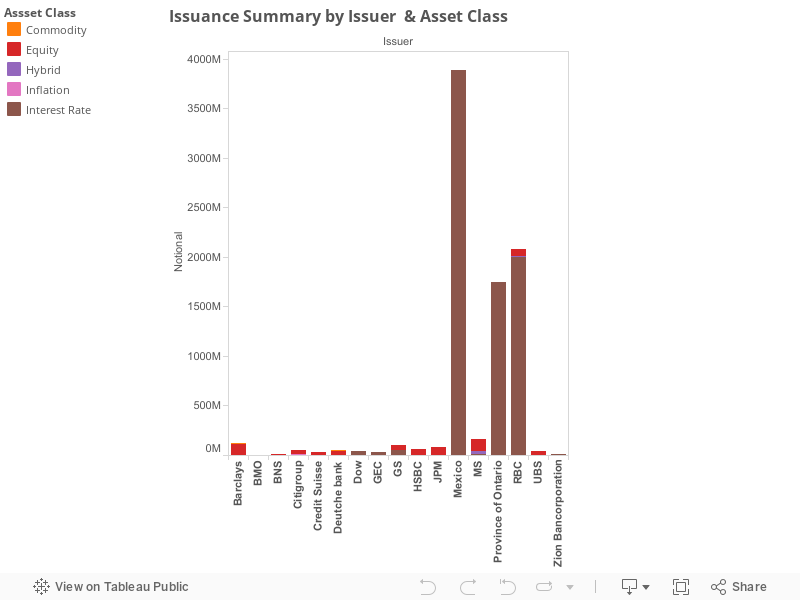

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

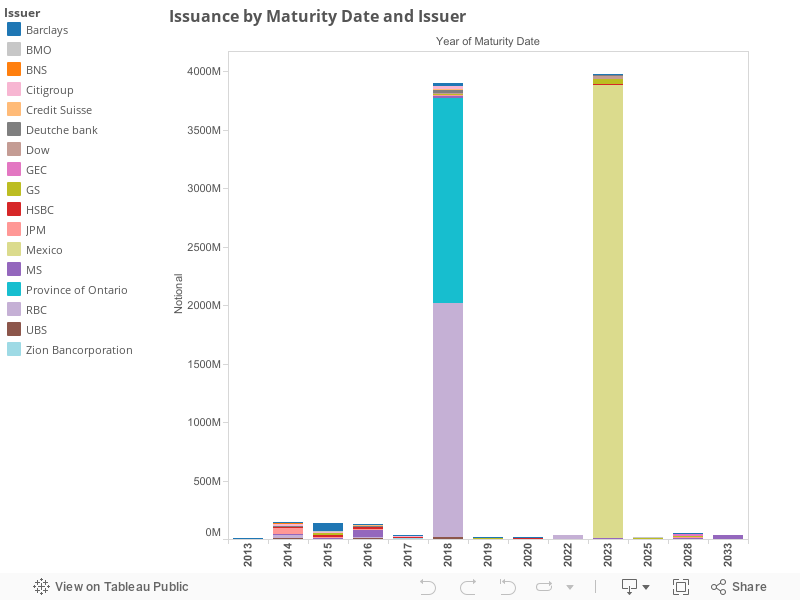

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2018. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2018. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

For additional details please refer to the Issuance summary table.

For additional details please refer to the Issuance summary table.

No comments:

Post a Comment