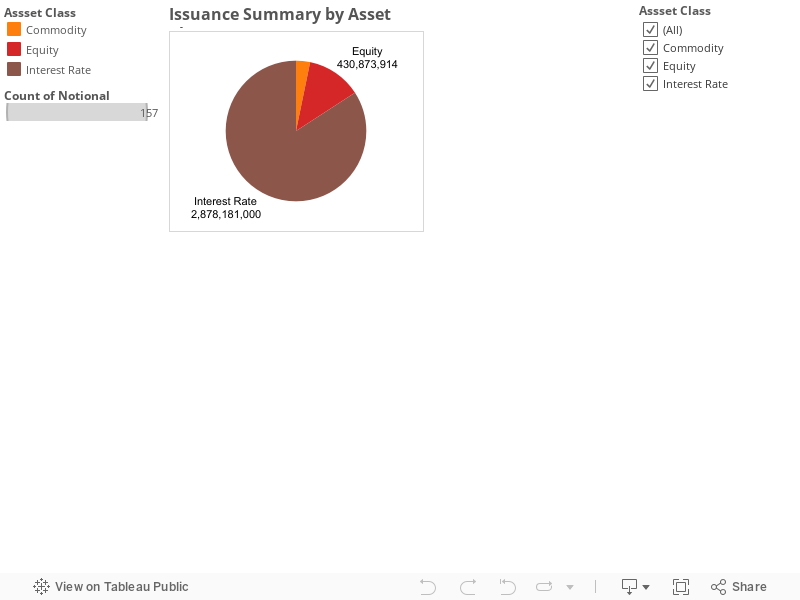

During the week of September 16-20, 2013 structured note issuance has been 3.4 BN across various issuers and asset classes. Most of the issuance (2.8 BN) is driven by Interest Rate linked notes and 430 MM of the issuance is driven by Equity linked products. Interestingly Commodity issuance has spiked this week. For Details of the distribution refer to the chart below. Surprisingly majority of the structured note issuance is linked to Interest Rate linked.

Interactive Issuance analysis

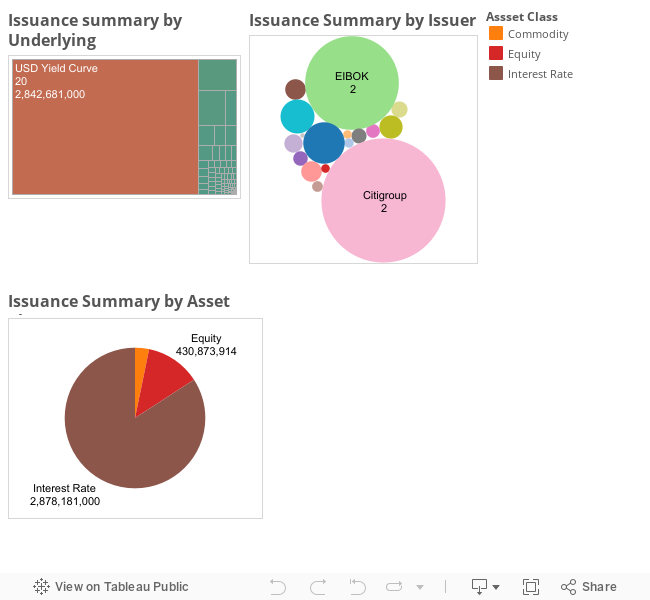

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

Interactive Issuance analysis

You can click individual asset classes to see how the underlying issuance has happened within each asset type by underlying and Issuer.

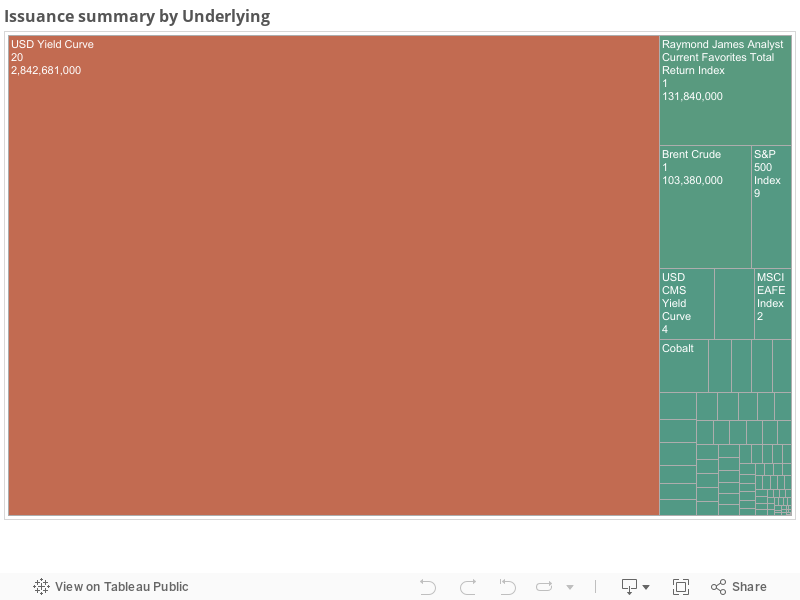

Underlying analysis

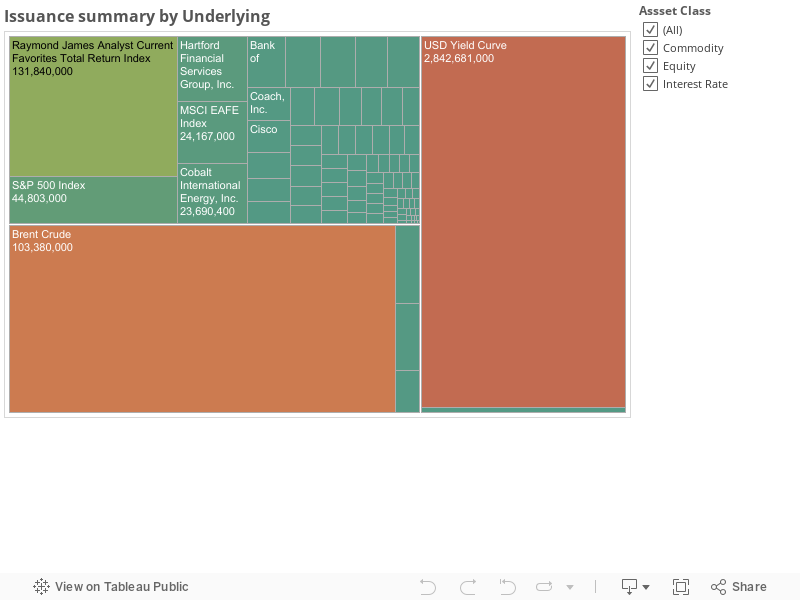

Underlying analysis

Citigroup has issued one large interest rate linked fixed rate notes. This note matures in september 2018. 1.7 Bn Fixed rates paying a coupon of 2.5 % and suitable for investors seeking to tap into the rising interest rates. This might not be a best deal for an aggressive investor but definitely better yields when compared to US 5Y Treasury

On the Equity linked notes front there has been good amount of activity. Scotia Bank leading the pack with 30.6 % market share.

Notably Scotia Bank issued a large note (128 MM) on Raymond James Analyst Current Favorites Total Return Index (Bloomberg Ticker: RJACFTR) to the investors.

The Raymond James Analyst Current Favorites Total Return Index (the “Index”) is a proprietary index that is intended to track the performance of the Raymond James Analyst Current Favorites List of stocks or other exchange-traded securities, on an adjusted basis. The rules for constructing and rebalancing the Index were developed by Raymond James & Associates, Inc. The Index level is calculated and published by Bloomberg LP (the “Index Calculation Agent”).

These notes belong to class of performance notes. They command the market performance without any cap. On the downside this note will participate in 1 to 1 downside. There is a possibility of losing entire principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

Citigroup has issued one large interest rate linked fixed rate notes. This note matures in september 2018. 1.7 Bn Fixed rates paying a coupon of 2.5 % and suitable for investors seeking to tap into the rising interest rates. This might not be a best deal for an aggressive investor but definitely better yields when compared to US 5Y Treasury

On the Equity linked notes front there has been good amount of activity. Scotia Bank leading the pack with 30.6 % market share.

Notably Scotia Bank issued a large note (128 MM) on Raymond James Analyst Current Favorites Total Return Index (Bloomberg Ticker: RJACFTR) to the investors.

The Raymond James Analyst Current Favorites Total Return Index (the “Index”) is a proprietary index that is intended to track the performance of the Raymond James Analyst Current Favorites List of stocks or other exchange-traded securities, on an adjusted basis. The rules for constructing and rebalancing the Index were developed by Raymond James & Associates, Inc. The Index level is calculated and published by Bloomberg LP (the “Index Calculation Agent”).

These notes belong to class of performance notes. They command the market performance without any cap. On the downside this note will participate in 1 to 1 downside. There is a possibility of losing entire principal. But If investors portfolios have captured market performance and think market performance would not be in single digits they can juice twice the returns with some protection. Definitely a good deal to think of!. There are other notes that were designed with S&P 500 and EURO STOXX 50 index. There are some interesting notes that are providing good return on the investment. Refer to the chart below for issuance of other underlyings.

There has been some issuance activity in Commodity and Currency segments of the markets.

Notable note issued by Barclays to capture performance of Brent crude oil. I guess middle east geopolitics play can be captured into your portfolio by entering into this contract. Barclays issued 103 MM worth of Brent crude oil based yield enhancement class structured note. These notes command a maximum of 15% if Brent crude oil rises and will participate 1:1 downside performance with risk of losing entire principal.

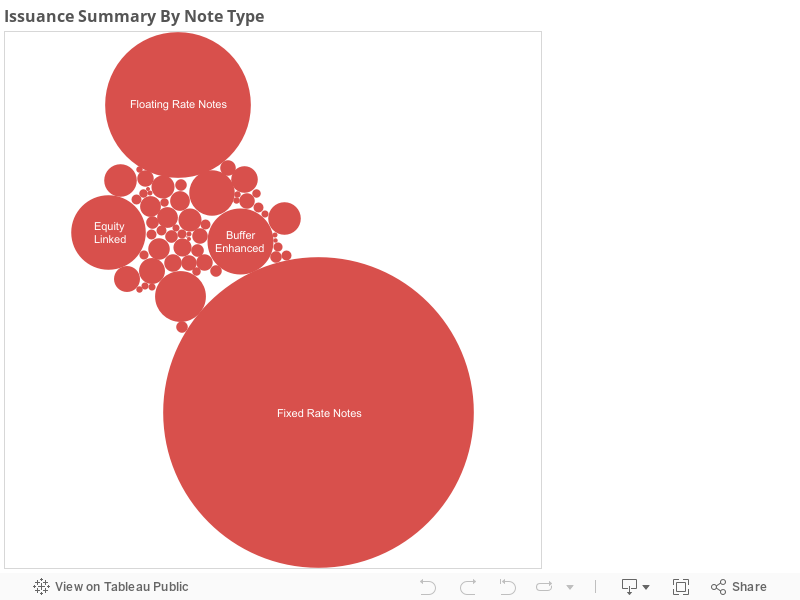

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

There has been some issuance activity in Commodity and Currency segments of the markets.

Notable note issued by Barclays to capture performance of Brent crude oil. I guess middle east geopolitics play can be captured into your portfolio by entering into this contract. Barclays issued 103 MM worth of Brent crude oil based yield enhancement class structured note. These notes command a maximum of 15% if Brent crude oil rises and will participate 1:1 downside performance with risk of losing entire principal.

Size of the note types will tell us an indication of what type structures are popular among the investors and where money is flowing. Below chart shows this theme

Popular notes have been Fixed Rate Notes, Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. This week market activity has been shadowed by one large issuance by Korean Development Bank.

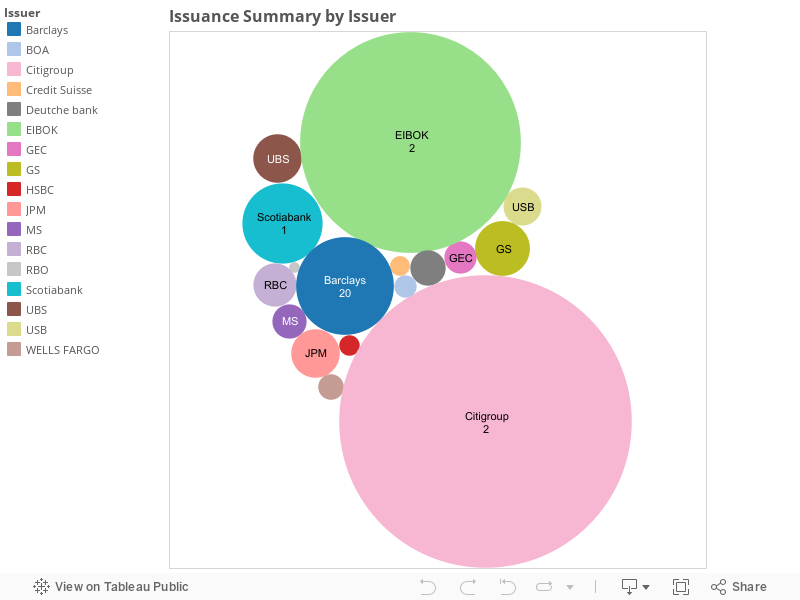

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week Citigroup with its large issuances of Interest Rate linked notes captured 50% of the issuance volume. EIBOK,JPM, RBC and GS captured rest of the issuance market share.

Popular notes have been Fixed Rate Notes, Floating rate notes. Two notes are Interest rate related notes designed to capture the performance in the Fixed income markets.This kind of activity could be due to surge in demand from investors to capture market gains as they view markets will witness rising yield environment. This week market activity has been shadowed by one large issuance by Korean Development Bank.

Now moving on to issuers side and understanding their market penetration or competitor analysis provides some interesting insights.

This week Citigroup with its large issuances of Interest Rate linked notes captured 50% of the issuance volume. EIBOK,JPM, RBC and GS captured rest of the issuance market share.

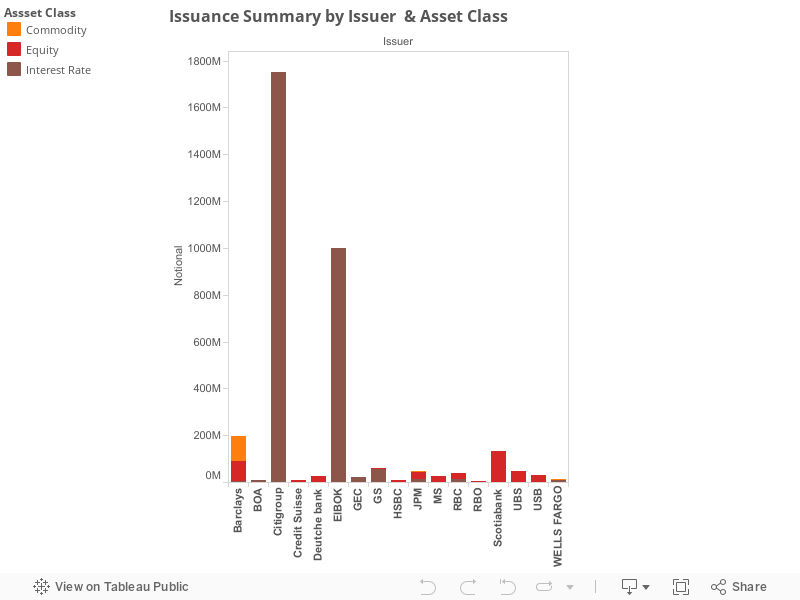

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

Market penetration is driven by the issuer depth in each of the asset classes. Every issuer has presence in Equity linked issuance. Goldman is only issuer to produce Currency related issuance. Morgan Stanley and JPM are active players in the Hybrid related issuance.

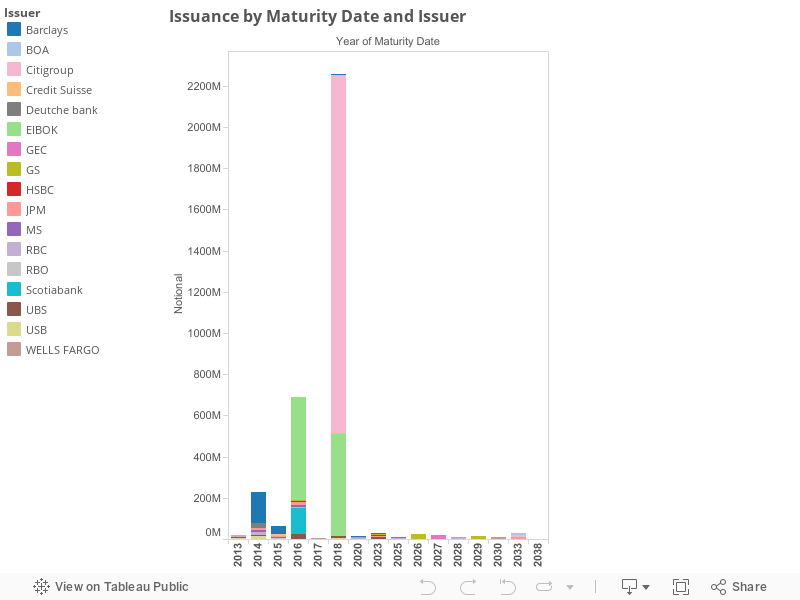

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2018. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

Maturity profile of the issuance by issuer provides where volumes are anchored. Interestingly most of the volume issued this week matures between 2014 and 2018. This can be attributed to two facts. Issuers are stretching the maturity of the note to come up with better coupons.

For additional details please refer to the Issuance summary table.

For additional details please refer to the Issuance summary table.

No comments:

Post a Comment